.svg)

Peoples Financial Corporation (PFBX) has delivered stable financial performance in recent years that is broadly consistent with its regional peers, although certain fundamentals have come under pressure more recently due to deposit declines and broader macroeconomic factors. At the same time, the dissident has not articulated any strategy for improving the Company’s operations or enhancing shareholder value. Therefore, we believe shareholders are best served by maintaining continuity and voting FOR all management nominees.

Peoples Financial Corporation (PFBX) operates as a community bank holding company through its subsidiary, The Peoples Bank, serving the Mississippi Gulf Coast market across Hancock, Harrison, Jackson, and Stone counties.

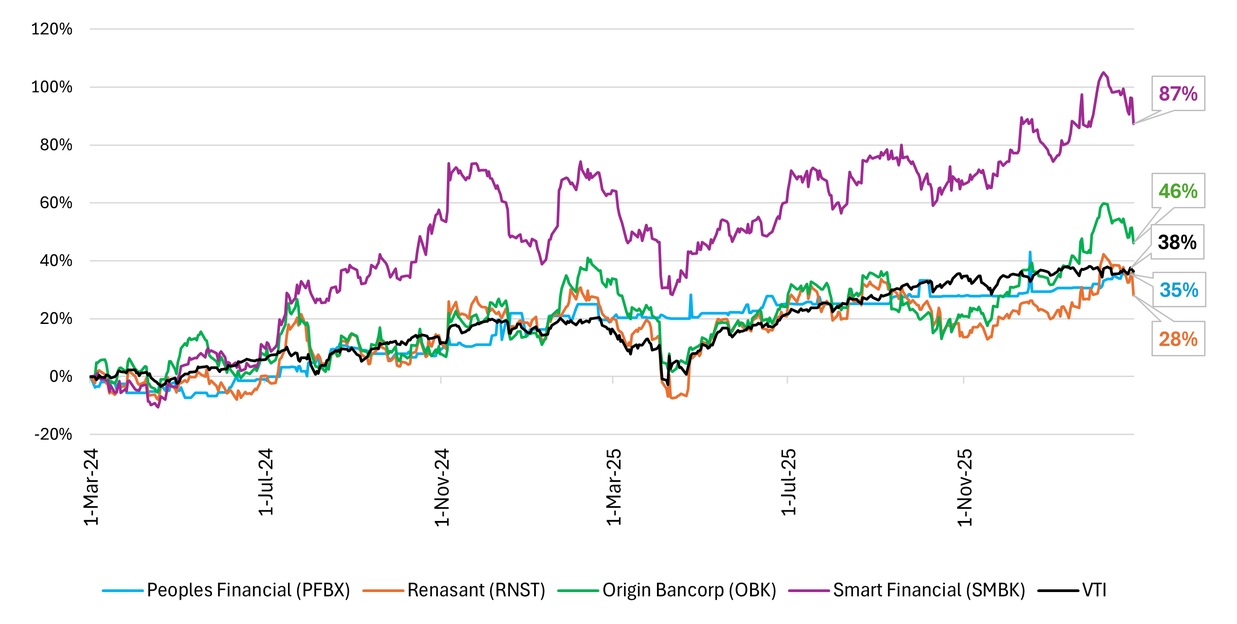

When compared to similarly situated regional banks, performance over the two- and five-year periods is broadly in line with peers. The Company has not materially underperformed peers in recent years, nor has it exhibited signs of operational instability.

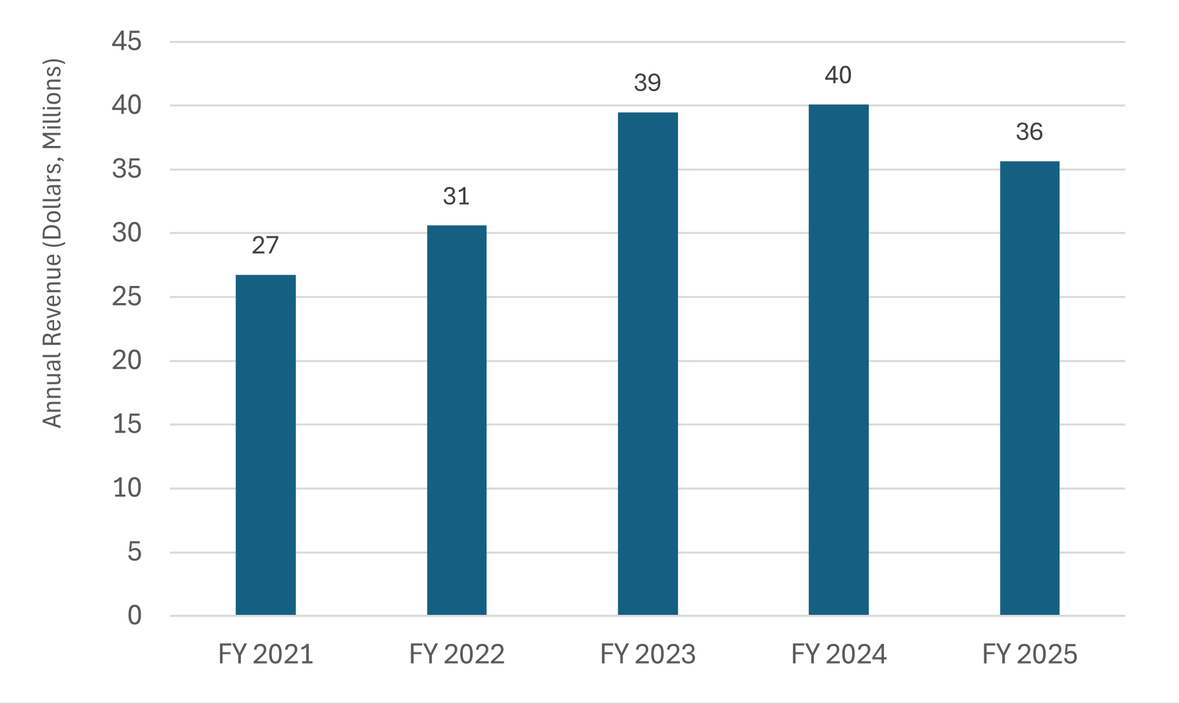

From a financial perspective, the Company’s fundamentals do not suggest a business in need of a turnaround. Revenue has generally trended upward over the past five years, although the upward trend has slowed down in recent years.

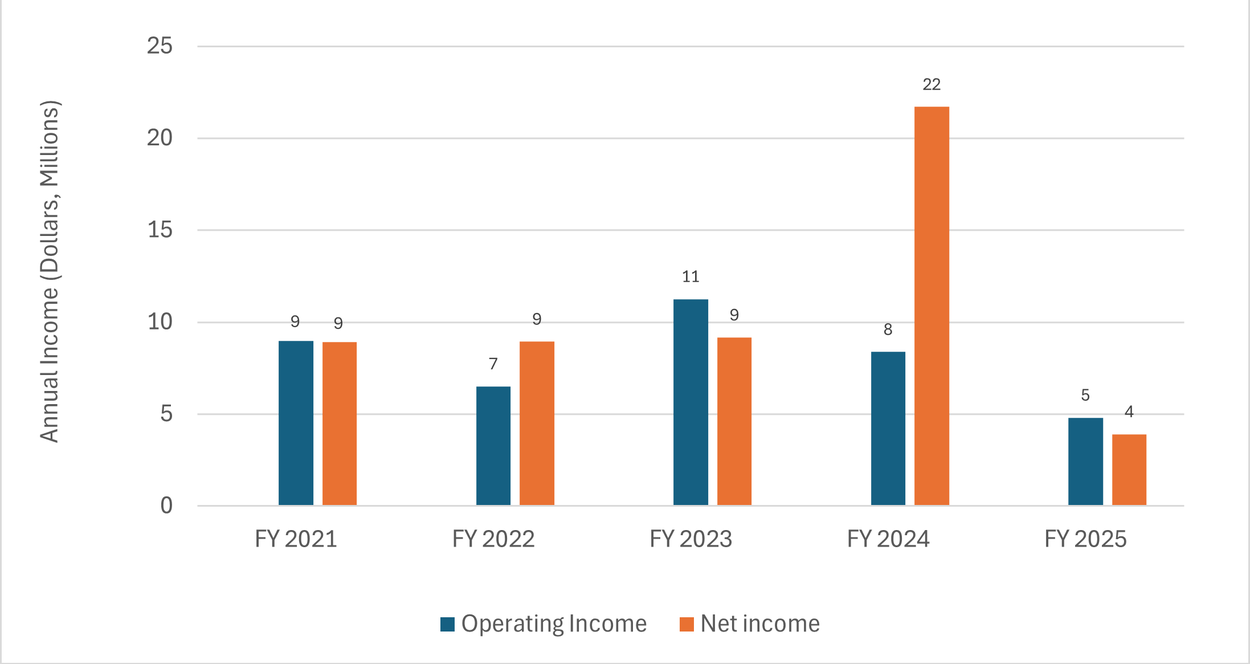

Earnings, however, have seen a decline in recent years, though margins remain healthy with net margin for FY 2025 sitting at 11%. The decline in operating income to $4.8 million in FY 2025 from $8.4 million in FY 2024 was driven primarily by shrinking asset balances and falling yields.

On the balance side, the Bank lost a significant volume of public fund deposit accounts to competing local banks through competitive bid processes, causing total deposits to fall by $116.3 million. With less funding available, balances in the securities portfolio and overnight federal funds contracted materially. On the yield side, the broader interest rate environment pushed earned rates lower across nearly all asset categories. This was most notably seen on overnight fed funds, which declined from 5.34% to 4.42%, and on the securities portfolio, where yields fell across both AFS and HTM holdings. Together, these two pressures reduced net interest income by approximately $3.1 million year over year.

The difference between reported net income of $3.9 million in 2025 and $21.7 million in 2024 is largely attributable to a one-time $15.2 million tax benefit recorded in FY 2024 from the reversal of the Company's deferred tax asset valuation allowance.

The Company's strategy centers on providing traditional banking services, including commercial, real estate, construction, personal, and installment loans, with a primary emphasis on commercial lending, to individuals, small and middle market businesses, and state, county, and local government entities within its trade area. The Bank maintains a strong core deposit base through interest-bearing and non-interest-bearing checking accounts, savings accounts, certificates of deposit, and IRA accounts.

Growth has been achieved primarily through internal means, including de novo branching and an emphasis on strong customer relationships, with only limited pursuit of external acquisition strategies. The Bank also operates a trust and investment services department offering financial, estate, and retirement planning services. The Company intends to continue its strategy of being a local community bank offering traditional banking services within its Gulf Coast trade area.

Stilwell Value has once again nominated Stewart F. Peck to the Board, continuing a multi-year campaign. However, as in past years, the dissident’s filings provide no discussion of how the Company’s operations should be improved, no recommendations regarding capital allocation, and no proposed strategic direction. The only substantive disclosure regarding the nominee is his professional background, which consists of a legal career rather than operational or banking leadership experience.

Shareholders are therefore being asked by Stilwell to support a board nominee without any information concerning the nominee’s vision for the Company. Furthermore, the dissidents do not raise any specific concerns about the Company’s current operating strategy.

While the dissident has not articulated a path forward, shareholder voting results suggest that investors are not without concerns. The Company’s most recent say-on-pay proposal received 63.8% support. This level of approval is below typical market standards and indicates a degree of shareholder dissatisfaction.

This figure is further impacted by the Company’s ownership structure. Chevis Swetman (the chairman & CEO) and A. Tanner Swetman (Chevis Swetman’s son and a VP at the bank) collectively control approximately 30% of outstanding shares. If these insider holdings are excluded, support from unaffiliated shareholders falls to approximately 48%, suggesting that the proposal would not have received majority approval from independent shareholders.

Following the vote, the Company has not disclosed any engagement with shareholders regarding the outcome, nor has it indicated any updates to its compensation policies. Therefore, under our Governance Policy, this level of support and the lack of response from management warrant a recommendation to vote against this year’s say-on-pay proposal.

While the Company’s long-term return profile is weaker relative to the broader market and the Bank has experienced volatility with earnings in recent years, the TSR of the Company is approximately in line with the middle of its peer group. Additionally, the fundamentals do not indicate that a radical turnaround is needed at the bank (in contrast to what has been needed with recent campaigns at Jack in the Box and Cracker Barrel). Introducing a director without a defined strategy, operational plan, or relevant industry experience would introduce uncertainty without a clear benefit.

We therefore recommend that shareholders WITHHOLD votes from the Stilwell nominee Stewart Peck and vote FOR all six management nominees.