.svg)

.png)

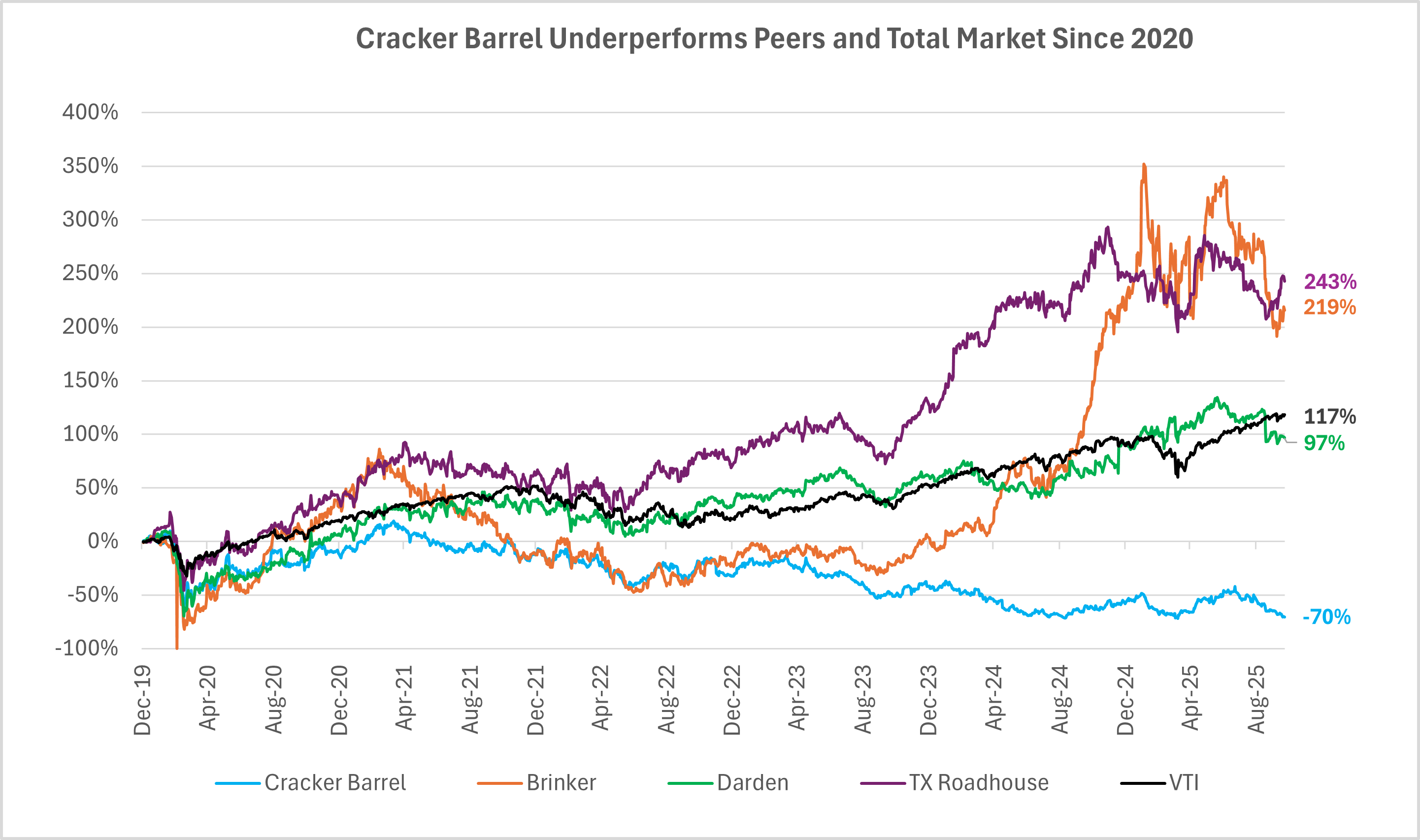

Cracker Barrel Old Country Store, Inc. (NASDAQ: CBRL) is a failing brand. Its market capitalization of approximately $730 million is at its lowest level since 2009, when the company was facing the fallout from the great financial crisis. Since early 2020 (pre-pandemic), Cracker Barrel’s total shareholder return (TSR) is -70%.

On November 20, 2025, shareholders will have a chance to vote on the Company’s directors (amongst other items). While the recent logo controversy is fresh in the mind of investors, Cracker Barrel’s challenges go far beyond the removal of the old-timer. Given the current decline of the Company, time is of the essence to reexamine strategy and save this storied brand before it is too late.

After engaging with both sides and analyzing Cracker Barrel’s performance, we recommend shareholders WITHHOLD votes from directors Berquist, Dávila, Ruiz, and Wade as well as CEO Julie Masino. This recommendation reflects continued underperformance marked by rising operating costs, declining traffic, and a sharp drop in earnings from pre-pandemic levels.

Over the past 5 years, Cracker Barrel’s total shareholder return (TSR) has significantly lagged Brinker, Darden, and Texas Roadhouse, as well as the broader market (VTI).

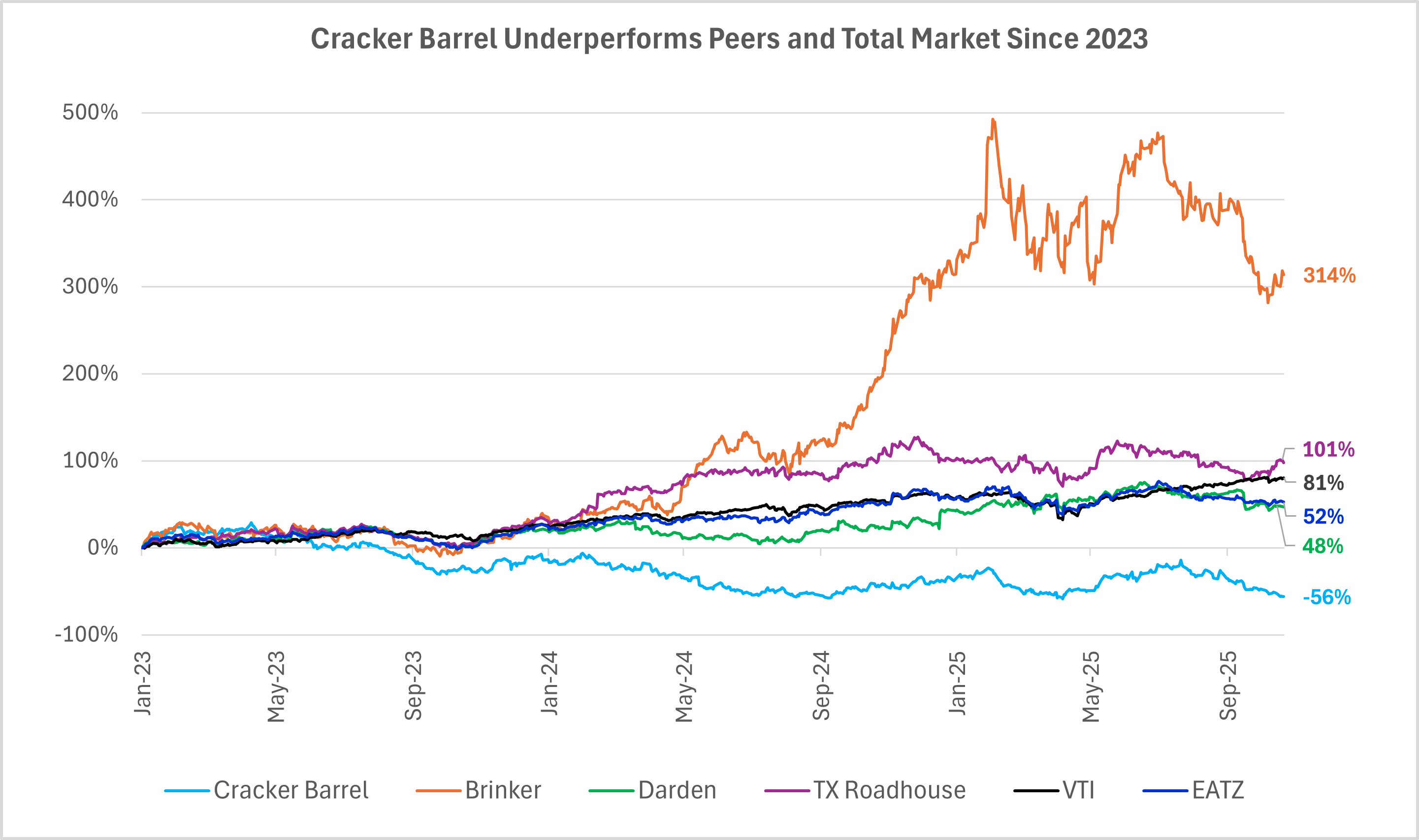

While peers rebounded since 2023, Cracker Barrel’s recovery never materialized (see charts below).

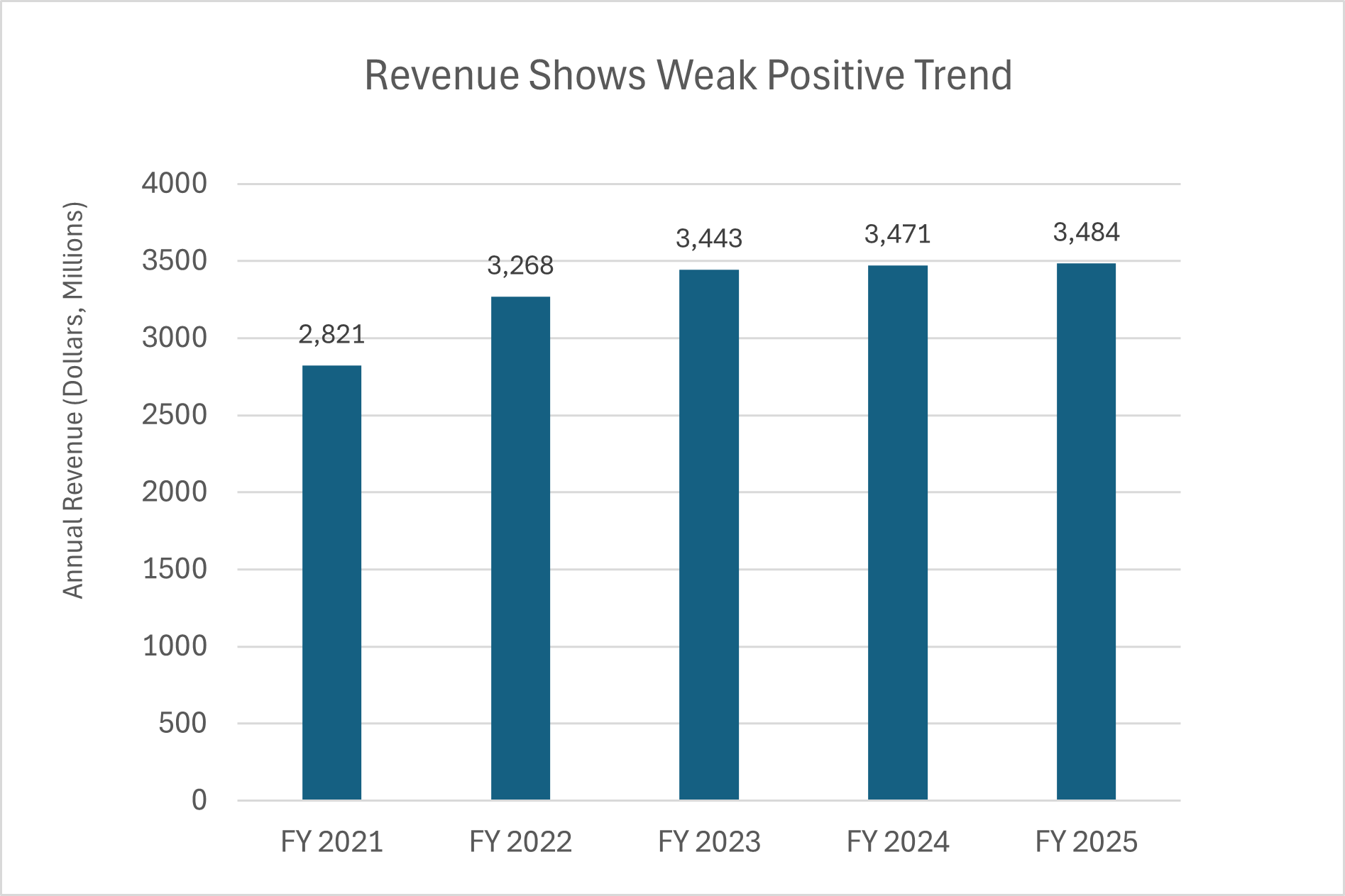

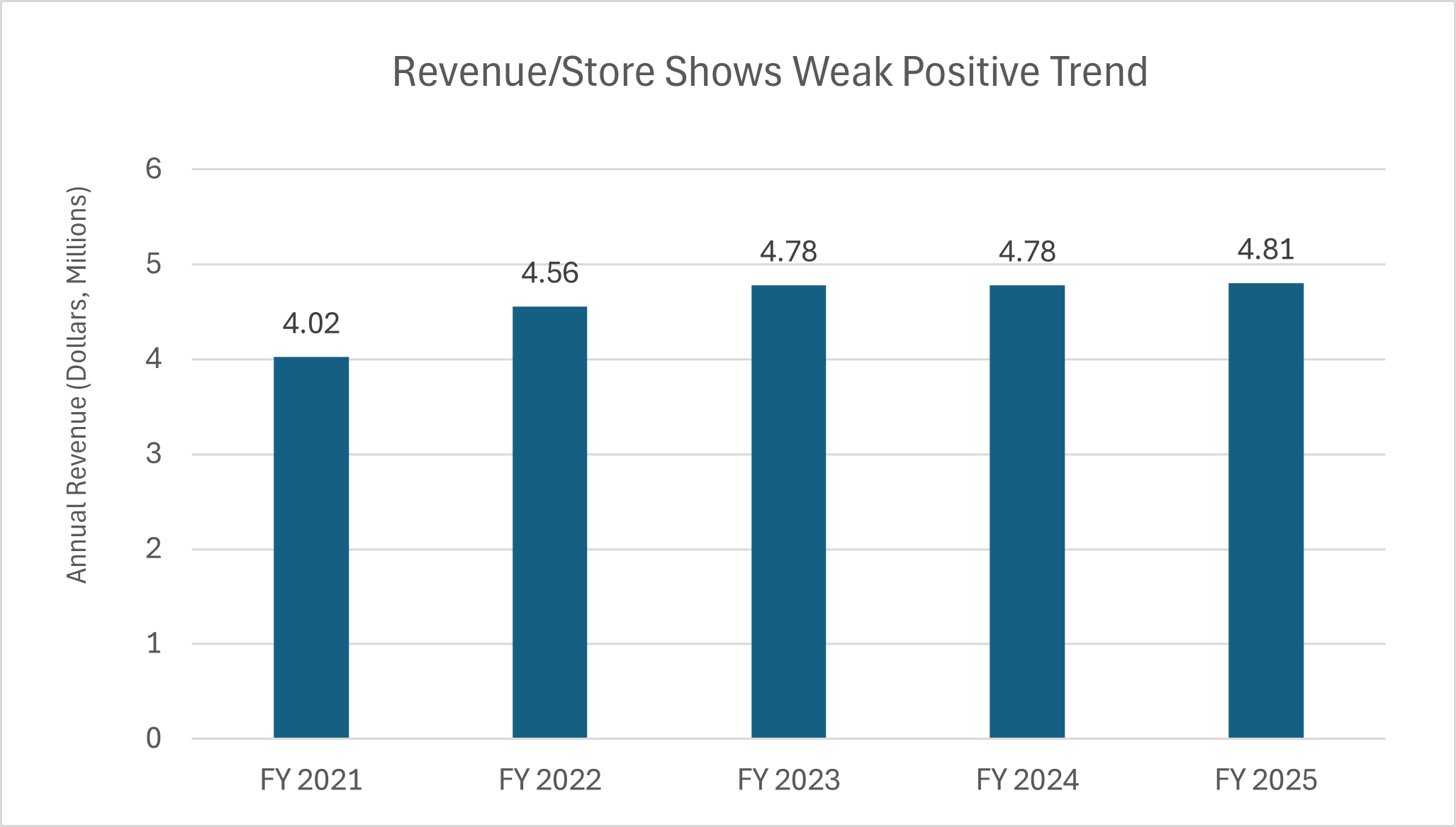

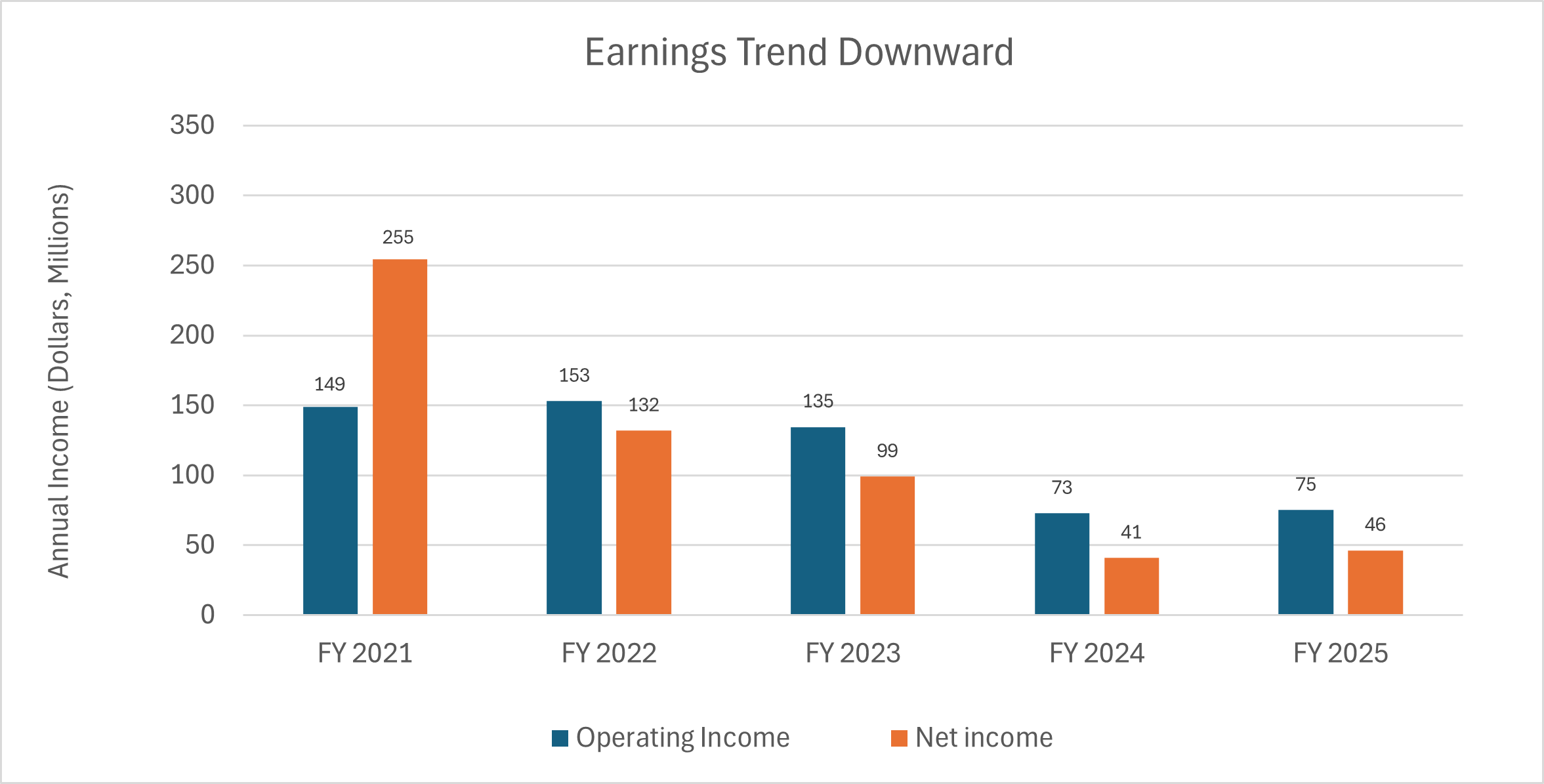

Revenue is up 7% since 2022 despite declining traffic (down 5% in FY2024 and 3% in FY2025). However, operating expenses have increased more rapidly, up 17% since 2022.

Over the same period, net income fell 65%, from $132 million in FY 2022 to $46 million in FY 2025. The net income picture is more bleak since 2021, falling 82%.

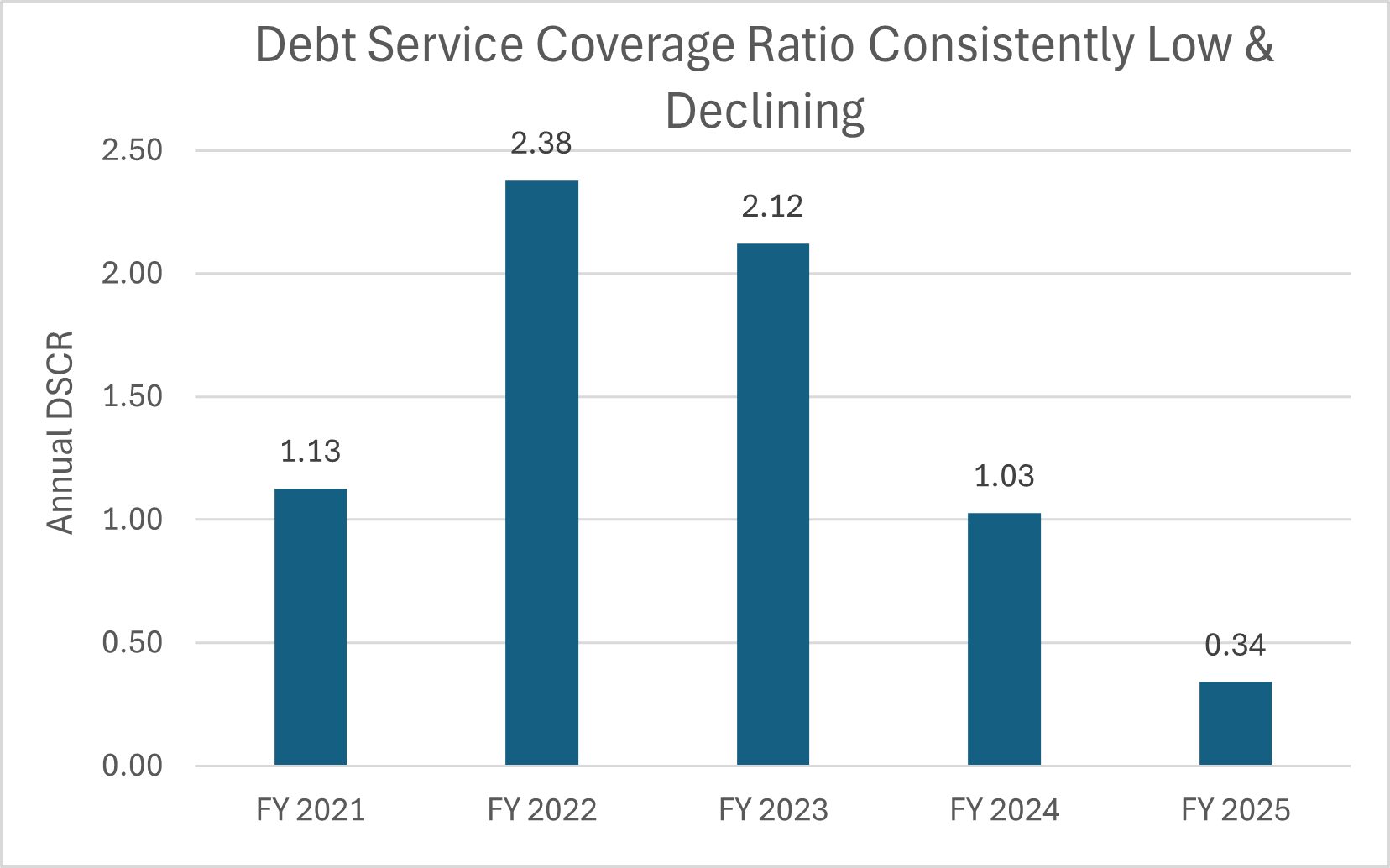

While debt levels remain moderate, declining earnings threaten Cracker Barrel’s ability to service debt. In FY 2025, the Debt Service Coverage Ratio (DSCR) fell below 1.0, indicating that operating earnings could not fully cover debt payments.

Some industries are characterized by high required capex and high fixed costs. These include airlines, car manufactures, hotels, and notably restaurants, among others.

These industries are particularly challenging because even small declines in demand can drastically reduce profits.

Cracker Barrel finds itself in a precarious position that is familiar to seasoned investors – if the firm does not make required capital expenditures to maintain and improve existing facilities, restaurants will fail to attract customers and earnings will continue to fall. Further, Cracker Barrel must continue to pay fixed costs (rent, utilities, salaries, insurance, etc.), which will continue to sap cash regardless of actions. This is a vicious cycle.

Of particular challenge to Cracker Barrel is changing consumer appetites (pun intended) and low barriers to entry for competition.

If the vicious cycle becomes critical, Cracker Barrel may no longer have the cash necessary for capital expenditures and will have no option but to sell assets (restaurants) or raise more capital. Therefore, time is of the essence for Cracker Barrel to reverse course.

On November 1, 2023 Ms. Sandra Cochran was succeed by Ms. Julie Masino as CEO, who previously served as President of Taco Bell International.

Cracker Barrel announced a Strategic Transformation Plan in May 2024 along with a reduction in their quarterly dividend to provide capital for the plan and avoid a vicious cycle.

Management of Cracker Barrel must drive performance across three key levers:

However, Cracker Barrel has not provided any public data demonstrating improvement in any of these metrics since launching its Strategic Transformation Plan. Poor performance is borne out in the financials, discussed earlier.

Rebranding was a core pillar of Cracker Barrel’s transformation strategy, falling under the “Refine the Brand” initiative. As part of this effort, the Company remodeled four stores, refreshed 58 stores, and introduced a new logo that replaced the iconic “old-timer” and barrel imagery with a simpler, modern design.

However, backlash was immediate and intense. Within a week, Cracker Barrel reversed course, reinstating its original logo and halting further rebranding efforts. The controversy resulted in an estimated 8% decline in traffic and a sharp drop in share price. Management stated that it had conducted thorough testing prior to rollout and did not anticipate such a strong negative response.

In response to the incident, the Company lowered its FY2026 guidance, projecting revenue between $3.35 and $3.45 billion and traffic declines of 4–7%, both representing deterioration from prior expectations.

It is important to note, however, that Cracker Barrel’s challenges pre-date the logo controversy and extend far beyond branding missteps. The Company’s underlying issues declining traffic, rising costs, and operational inefficiencies — have persisted for years. Indeed, one could argue that the publicity surrounding the rebranding may have had a minor silver lining, as it briefly renewed public awareness of the brand among consumers who had not engaged with Cracker Barrel in years.

Cracker Barrel faces deep structural and strategic issues declining traffic, rising costs, and poor execution. While management’s initiatives may show intent, execution has faltered.

Management has yet to identify the root causes of rising operating costs or declining guest traffic, and shareholder returns have remained negative since the plan’s introduction.

Given the company’s weak FY2026 projections and the continued destruction of shareholder value, we recommend withholding votes from long-tenured directors; Berquist, Dávila, Ruiz, and Wade as well as CEO Julie Masino, under whose leadership shareholders have lost approximately $1 billion in value.