.svg)

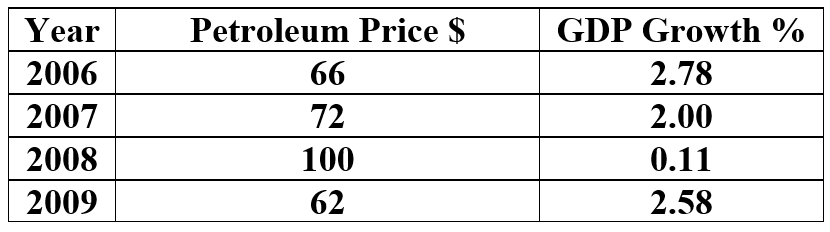

For the past 100+ years, petroleum availability and prices have had a major impact on the economy. Today is no different. For the benefit of sophisticated institutional investors and risk managers, we aim to address items related to the reopening of the Strait of Hormuz (see comments on the impact on industries below).

One must look no further than this year’s equity markets and the 2008 Credit Crisis to see the impact of energy prices on the economy.

While one could argue that petroleum is less critical than it was approximately two decades ago, there is little doubt that it remains highly relevant.

As is typically the case during wartime, the reporting is heavily skewed. During both Vietnam and Afghanistan, the public was led to believe that just a bit more effort would turn the tide. Our view is that Israel and the U.S. cannot force a regime change even if they were willing to place thousands of troops on the ground, which of course they are unwilling to do. Furthermore, it is unclear how the U.S. and Israel can force the re-opening of the Strait of Hormuz. Lastly, given the fact that logistics typically win, Iran can easily be re-supplied, and the U.S. and Israel cannot, it appears that Iran has the upper hand.

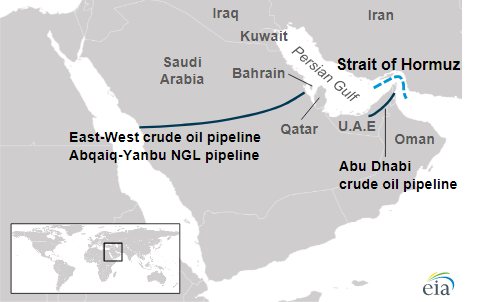

THE issue that much of the world is focused on is the re-opening of the Strait of Hormuz. While there is little doubt that Israel and the U.S. have done much to degrade Iran’s military capacity, they apparently have not destroyed the enriched uranium, nor have they destroyed all the missiles, drones, and small attack boats capable of attacking oil vessels. Given the dispersion of Iran’s weapons, it is doubtful that these weapons could be destroyed. If the tankers were escorted by military vessels, the escorts along with the tankers are likely to become vulnerable. Note, there has been talk of mining the Strait, but doing so might make the Strait impassable for any type of vessel, including those carrying crude to Iran’s allies.

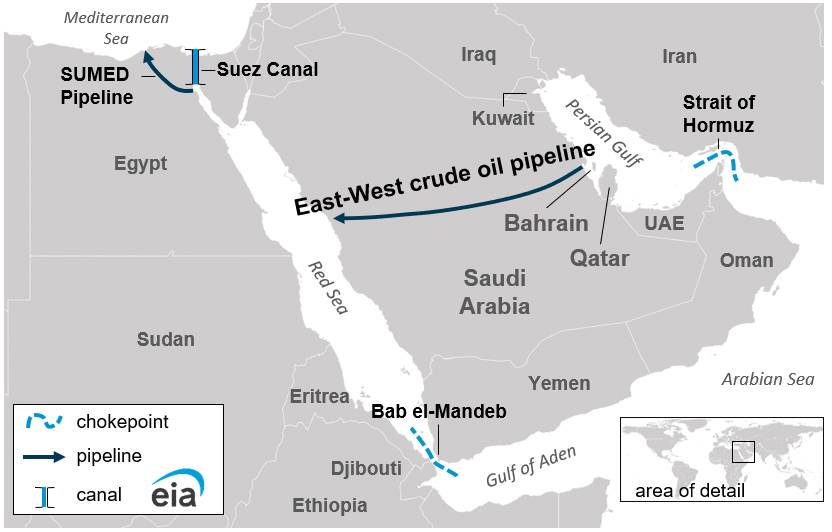

A possible mitigant is the transfer of oil to the Red Sea (and Suez Canal) via the East–West Crude Oil Pipeline. This will help, but only at the margin as the pipeline can only carry 5M barrels of crude per day compared to normal shipments through the Strait of Hormuz of 20M barrels per day.

Ukraine has been dealing with Shahed drone and missile attacks for the past several years with some success. However, the situation on the Strait is different in the sense that even if one in four attacks is successful, it will probably be sufficient to make vessel insurance rates prohibitively expensive, and Iran has multiple tools for the attacks: drones, missiles, and fast boat delivered missiles and torpedoes.

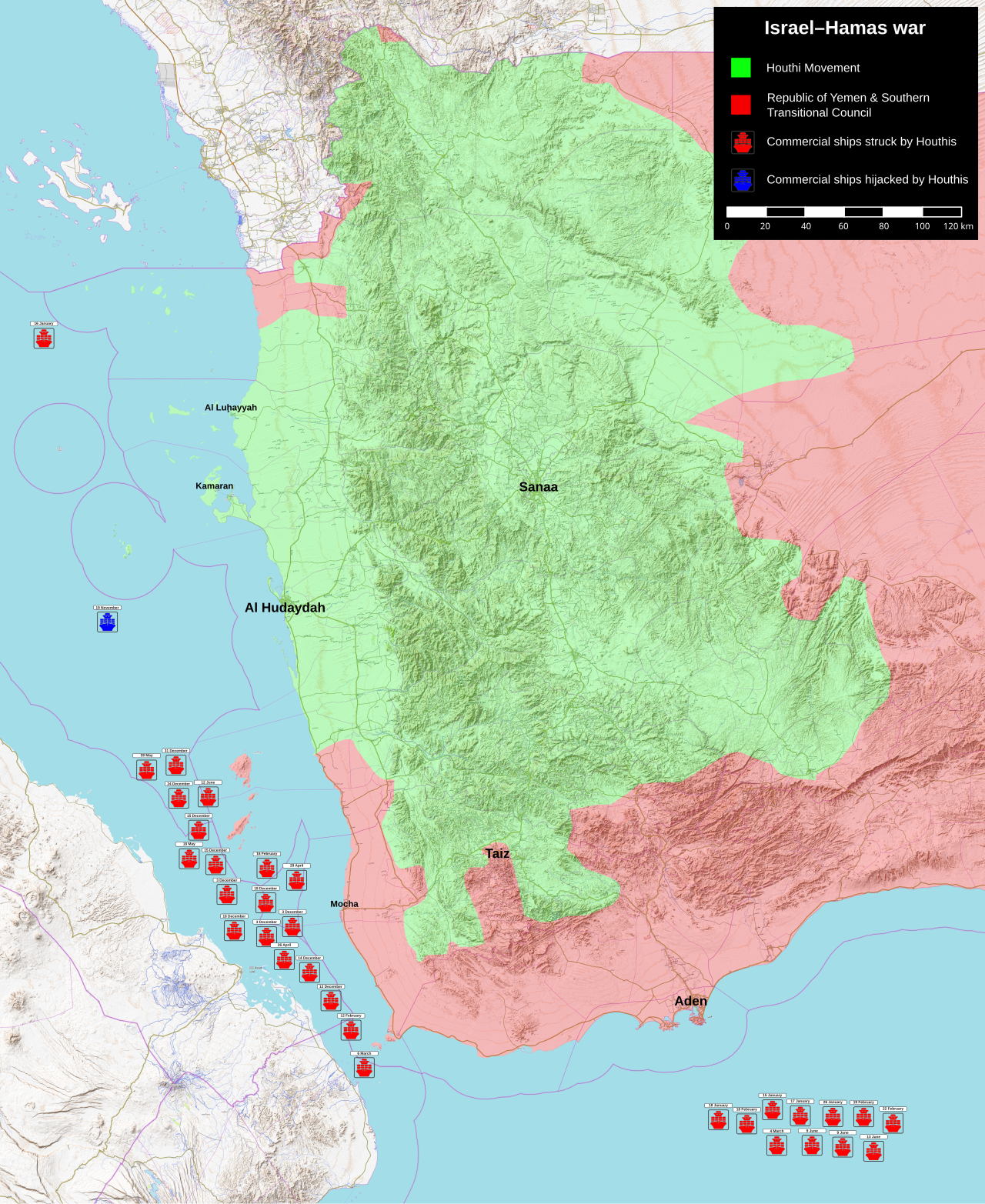

A major challenge in any war is anticipating the next move of one’s opponents. Lest we forget, Iran’s Houthi allies, based in Yemen, have previously attacked ships heading south in the Red Sea. Approximately 4M barrels per day flow through the Bab el-Mandeb Strait.

Since 2023, the Houthis have attacked 178 vessels.

To effectively predict the action of various parties, it helps to understand their objectives/ motivations. Below is a summary:

Iran Leadership – continue its existence as an independent state, end the sanctions, and be allowed to develop nuclear weapons, which it presumably believes will ensure its sovereignty. Over time, drive the U.S. out of the Middle East and deepen relationships with rebel groups across the region (Hamas, Houthis, Hezbollah, Shiite militias in Iraq, etc.)

Israel Leadership – regime change and the elimination of Iran’s military capacity and its nuclear capabilities.

U.S. Leadership – regime change and the elimination of Iran’s military capacity and its nuclear capabilities.

Russia – maintenance of high energy prices, divert U.S. resources from Ukraine.

China – distract the U.S. from east Asia, see U.S. debt grow, and undermine its leadership position.

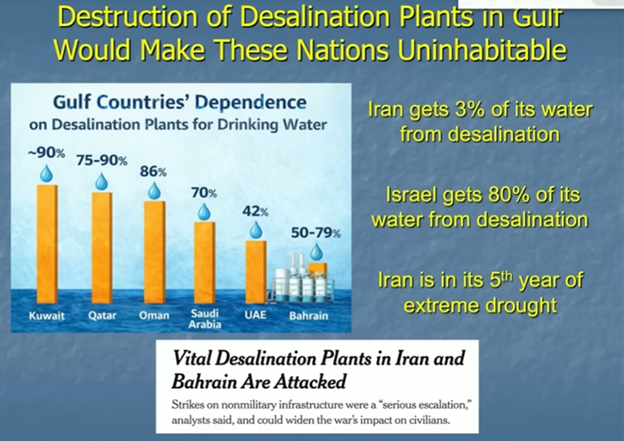

As is usually the case, war is extremely expensive with cost estimates near $1B per day. If the objective from the U.S.’s perspective was the elimination of Iran’s enriched uranium and regime change, those objectives appear increasingly unlikely. Our sense is that the U.S. likely has the least interest in its continuation and if it continues long, the public’s ambivalence will be reflected in the midterm and 2028 elections. On the energy front, the U.S. could halt the export of its energy, but such an action is likely to alienate major allies and domestic producers. Hence, a possible (perhaps increasingly likely) outcome is the U.S. claiming its mission has been accomplished and leaving others to clean up the mess. From the U.S.’s perspective, the concern will be one of losing bases as the Gulf countries might view having the bases as more of a risk than a benefit. The attacks on refineries and desalination plants are highly disruptive:

While a focus on winning is typically the goal in any endeavor, there are actions which are so unpalatable that their occurrence has long-term consequences. In this conflict, attacking the desalination plants, which the population of several Gulf countries are dependent on, will probably be perceived as unacceptable. Likewise, the assassination of sovereign/religious leaders probably fits in the same category and might be counterproductive.

Below is a preliminary assessment of the impact of the continued war on various industries (in order of impact):

Negative: Airlines, Automobiles, Trucking, Chemicals, Construction, Consumer Finance, Electric Utilities, Banking, Gas Utilities, Hotels, Restaurants & Leisure, Metals & Mining, Retail

Positive: Defense (particularly those focused on new tech), Energy, Energy Services, Cybersecurity

Wars change countries and change politics. Our view is that this war is likely to be the defining moment for the current administration. For sophisticated institutional investors and risk managers, we have identified some of the consequences, but expect more as conditions develop.