.svg)

While the market's attention has been fixed on the Middle East, record AI capital spending, and fresh index highs, a quieter and arguably more consequential development has been building beneath the surface: a political realignment toward the left. It is tempting to file it under local color or generational mood. We think that would be a mistake. The pattern rhymes with something the industrialized world has lived through before, and the last time it ran its course it reshaped tax policy, labor law, and the relationship between capital and the state for the better part of a century. As usual, this installment is written to give sophisticated institutional investors and risk managers a framework for evaluating a fast-moving development, one that is economic and political at once.

On June 30, Melat Kiros, a 29-year-old democratic socialist and first-time candidate, unseated Representative Diana DeGette in the Democratic primary for Colorado's 1st Congressional District, which covers Denver.1 DeGette had held the seat for roughly thirty years. Kiros ran on working families, universal health care, child care, and elder care, refused corporate PAC money, and campaigned against "the oligarchy."

A single primary would be easy to wave away. Several in a row, on the same platform, are harder to dismiss, and they point in one direction. Kiros' win followed a run of victories by candidates aligned with the Democratic Socialists of America: three winners in New York City primaries the week before, all endorsed by Mayor Zohran Mamdani, and a DSA-backed win in a Philadelphia-area district in May.2 The consistency of the platform across these races is the tell. A string of local upsets is better understood as a single current running through the electorate, and currents of this kind carry a history.

To understand where this current comes from, it helps to revisit where it came from the first time. The economic historian Robert Allen coined the term "Engels' Pause" to describe Britain from roughly 1790 to 1840, the first wave of the Industrial Revolution.3 He named it after Friedrich Engels, who documented the period in "The Condition of the Working Class in England" in 1845. The defining feature was a divergence: output per worker climbed steadily while the real wages of the working class went nowhere. Between 1780 and 1840, output per worker rose about 46% while real wages rose only about 12%.4 The rate of profit doubled, and labor's share of national income fell steadily, from roughly 56% around 1800 toward the mid-40s by 1860. The gains of the machine age accrued overwhelmingly to the owners of the machines.

That divergence spilled quickly into politics. Engels and Karl Marx published "The Communist Manifesto" in 1848, the year revolutions swept across Europe. In Britain, the Chartist movement organized the working class around political reform, and the trade-union movement gathered force once the Combination Acts were repealed in the 1820s. A generation of stagnant wages beneath rising output turns out to be a dependable recipe for a leftward political shift.

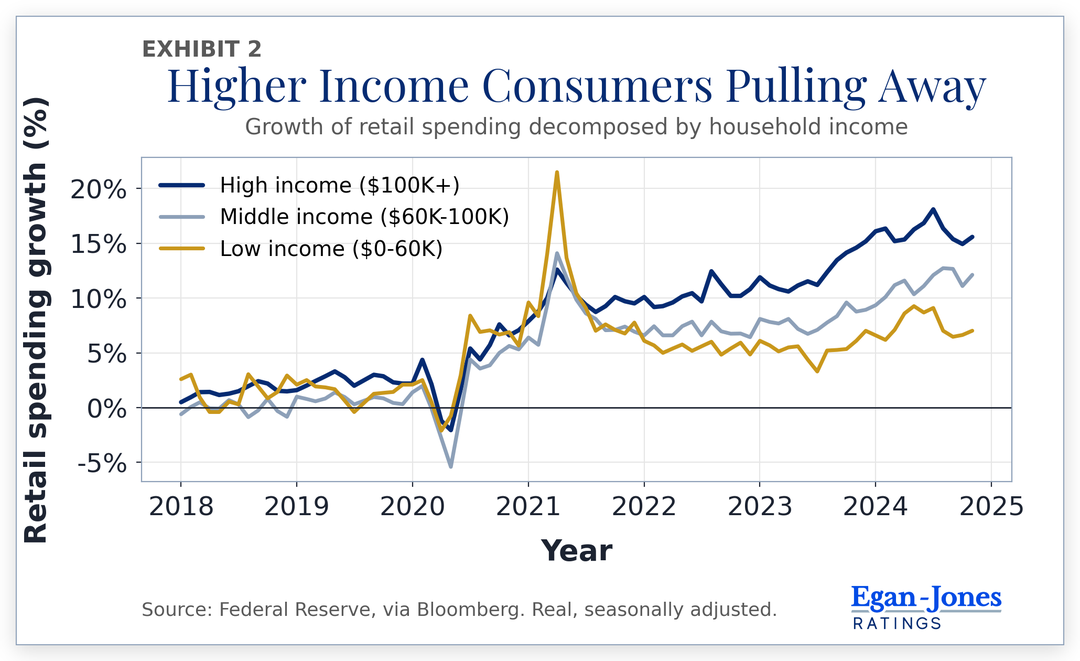

The modern signature of the same phenomenon travels under a different name: the K-shaped economy. It has moved well past hypothesis. One consumer-research firm now calls it "the defining structure of today's marketplace."5 The Federal Reserve Bank of New York finds that consumer spending diverged sharply after 2023, when pandemic-era subsidies expired, with only high-income households posting consistent real spending growth and the gains concentrated in luxury categories.6 Wealth has risen most at the top while cumulative inflation has weighed most heavily on the bottom.7 The Atlanta Fed describes a bifurcated recovery, with both groups' spending rising but at sharply divergent rates.8

The lower leg of the K is where the strain shows. Borrowers have increasingly sorted into superprime and subprime extremes, lower-income households are carrying heavier debt loads with rising debt-to-income ratios, and auto-loan delinquencies among them have been climbing.9 The tax changes enacted this year, whose benefits skew toward higher earners, are widely expected to entrench the divergence further.10 Swap "the machines" for "the algorithms," and the shape is the one Engels described: the top pulling away while the bottom runs to stand still.

The engine this time is artificial intelligence, and it is doing to cognitive work what mechanization did to craft labor. The warnings are pointed. Anthropic's chief executive has suggested AI could eliminate as much as half of entry-level white-collar jobs and push unemployment to 10-20% within one to five years.11 A Stanford study found that employment among early-career workers in AI-exposed occupations has fallen about 16% since late 2022.12 Goldman Sachs estimates roughly 6-7% of workers could be displaced over a decade of adoption, with entry-level workers in their twenties and thirties most affected, and wage growth for those workers has already slowed relative to less-exposed fields.13 The head of the largest US bank has said he expects to hire fewer people as a result.14

Here is the nuance that matters, and it is easily missed. The damage on the ground so far is modest and genuinely contested: Yale's Budget Lab found no overall change in employment for AI-exposed occupations, a National Bureau of Economic Research survey found little measurable effect to date, and a good deal of what gets blamed on AI is ordinary cost-cutting dressed in fashionable language.15 A large share of the political energy is aimed at the disruption people anticipate from AI, running well ahead of what the labor data has so far confirmed. The projections of mass white-collar displacement are louder than the current evidence, and that anticipation, broadcast by the very executives building the technology, is feeding the anxiety and, in turn, the politics. When the people constructing the machine tell the public that half its jobs may be gone within five years, they should expect the public to start voting on it.

The economic mechanism deepens the divide. Productivity gains accrue to the workers who can wield AI to augment complex, high-value work, and above all to the owners of the capital, the chips, the data centers, and the models. The worker whose task the model simply performs captures little of the gain. That is capital's share climbing at labor's expense, a twenty-first-century Engels' Pause compressed from fifty years into perhaps a single decade. The parallel is not ours alone; economic historians studying the period explicitly hold up the British experience as a warning light for the age of AI.3

The useful part of the analogy is the prognosis, because the first Engels' Pause resolved, and the manner of its resolution repays study. Marx's forecast revolution never arrived. The pressure worked itself out through a combination of forces. Real wages began to climb with productivity after the middle of the century, as capital accumulation caught up with the new technology's demands, and alongside that market adjustment the state was rewired: unions were legalized and grew, factory legislation curbed the worst practices, and the franchise widened through successive Reform Acts.

The sharpest illustration comes from Germany. Otto von Bismarck, no friend of the left, first tried to crush the socialist movement with an Anti-Socialist Law in 1878. When repression failed, he changed tactics and built the world's first welfare state, expressly to pull support away from socialism: health insurance in 1883, accident insurance in 1884, and old-age and disability pensions in 1889.16 A conservative chancellor had concluded that the cheapest way to preserve the existing order was to give labor a material stake in it. The United States reached a comparable destination a generation later, by way of the Progressive Era, the federal income tax in 1913, antitrust enforcement, and eventually the New Deal.

For investors the lesson is directional: when the divergence between capital and labor becomes politically intolerable, policy turns toward redistribution and toward the regulation of capital. The valuable analytical work lies one step further on, in the second-order effects, which in this domain tend to swamp the first-order ones. A policy's stated goal and its eventual incidence are frequently different things, and it is the incidence that moves credit and equity. The table below reads the likely policy vectors through that lens.

.png)

From our vantage as observers of credit, the nearest-term watch item sits at the bottom of the K, where consumer credit quality is already softening and where AI-driven wage compression would be felt first. Further out, the tax and spending channels above will move the trajectory of sovereign, municipal, and corporate credit alike.

A dose of humility is in order. The timing of political shifts is notoriously hard to call, and movements stall as often as they surge; in the same week as Kiros' win, an incumbent senator in her own state fended off a progressive challenger.1 The AI-labor data is early, noisy, and disputed, and the "half of all entry-level jobs" figures are forecasts of a technology still early in its diffusion, which is to say they carry wide error bars. History rhymes, and it keeps its own calendar; the first Engels' Pause took the better part of two generations to resolve. Our aim here is to recognize the configuration, a technological upheaval feeding a widening divergence feeding a political reaction, as one that markets have navigated before. The precise election or statute is beyond anyone's forecast.

The world is changing rapidly. A technology is concentrating the gains of growth in the hands of capital and the political winds are shifting in response. This installment aims to provide a framework of possible major shifts for the benefit of sophisticated institutional investors and risk managers. The more reassuring note from history is in how the first Engels' Pause resolved: through reform and, as capital accumulation caught up with the new technology, through wages that eventually rose with productivity again. The intervening adjustment was neither smooth nor cheap, and it is that adjustment for which investors would do well to prepare now.