.svg)

.jpg)

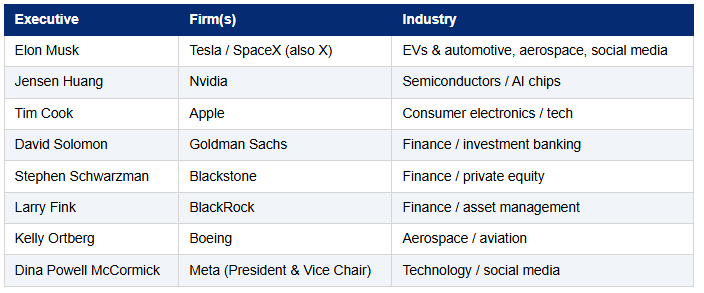

President Trump was joined by approximately 18 senior business leaders (Tim Cook, Elon Musk, Larry Fink, etc.)1 on his trip to China. The obvious question is what was discussed and why was he joined by the business executives. Perhaps the even larger issue is what the event means for the investment environment over the next couple of years, and who are the winners and losers.

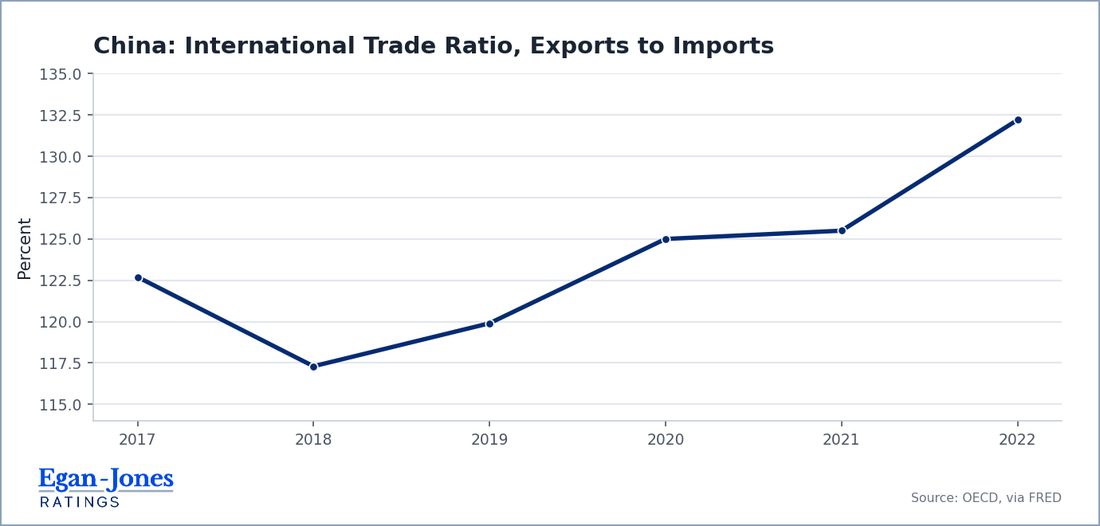

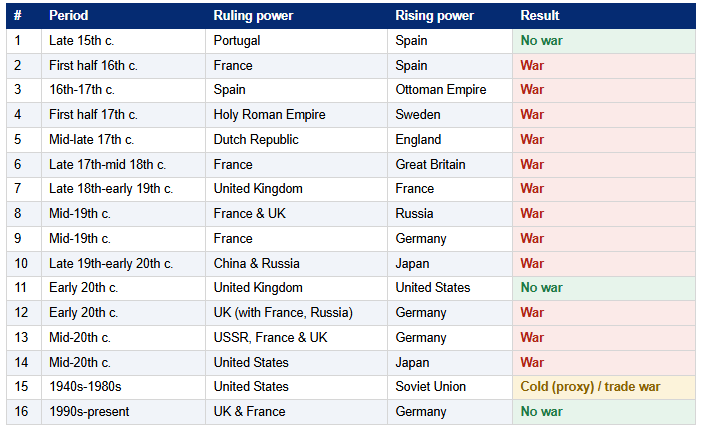

The “Thucydides Trap” is a description of the peril caused by the challenging of a regional leader by another. (See Appendix A for a summary of cases.) In the meantime, below is a chart indicating the trade imbalance with China.

As expected, both Trump and Xi are trying to solve their respective problems.

A major focus of the current administration is increasing jobs, which generally means an expansion of production on American soil. The change will boost employment, increase tax revenue, improve military readiness, and moderate debt relative to GDP. A “win” for the administration is garnering numerous orders for American goods and an agreement by China to invest in the US.

The major problems Xi faces are a relatively closed market for exports to the US, a faltering economy, concerns about energy accessibility, and access to advanced chips. There is also the always-present attempt to gain some control over Taiwan.

We have been here before with the concerns about Japan's dominance in various exporting areas (autos and electronics, mainly). The “solution” was to depress the dollar relative to other currencies, thereby boosting US exports. Perhaps the Accord was too successful, as Japanese exports collapsed and the Japanese government responded by reducing interest rates, increasing government spending, and making credit easier to obtain. The result was an asset bubble which, upon bursting, caused Japan to lose several decades of growth. Note, there is a contrary view on the Plaza Accord, and that is the dollar depreciated once the Fed reduced interest rates (from 12 to 6%), which had previously been set at high levels by Paul Volcker to fight inflation.

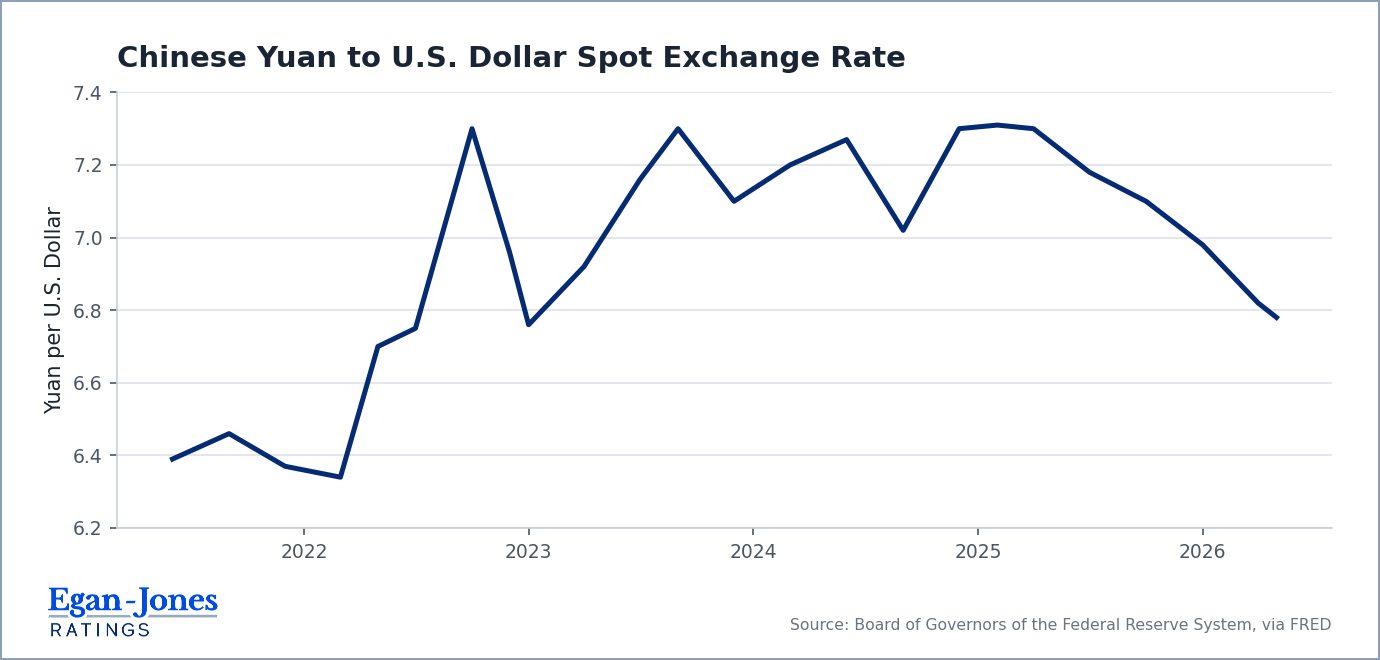

While in Plaza Accord I the problem was a supposedly strong dollar relative to the Japanese yen, it is not so apparent that the Chinese yuan is in a similar position, as shown below. Hence, we are not sure attacking the exchange ratios will cure the “problem”. Nonetheless, the problem remains and there are likely to be some significant adjustments. For starters, we expect China will make significant investments in the US. Just as after Plaza Accord I, Japanese manufacturers established manufacturing plants in the US, we expect the same from Chinese firms. Additional developments are probably agreements from China to purchase goods from US manufacturers such as Boeing airplanes and additional chips.

So, who might be the losers from the pending changes? Our view is that any industry which was protected in the US by effective trade barriers is likely to be harmed if Chinese manufacturers open facilities in the US. Below is a partial listing:

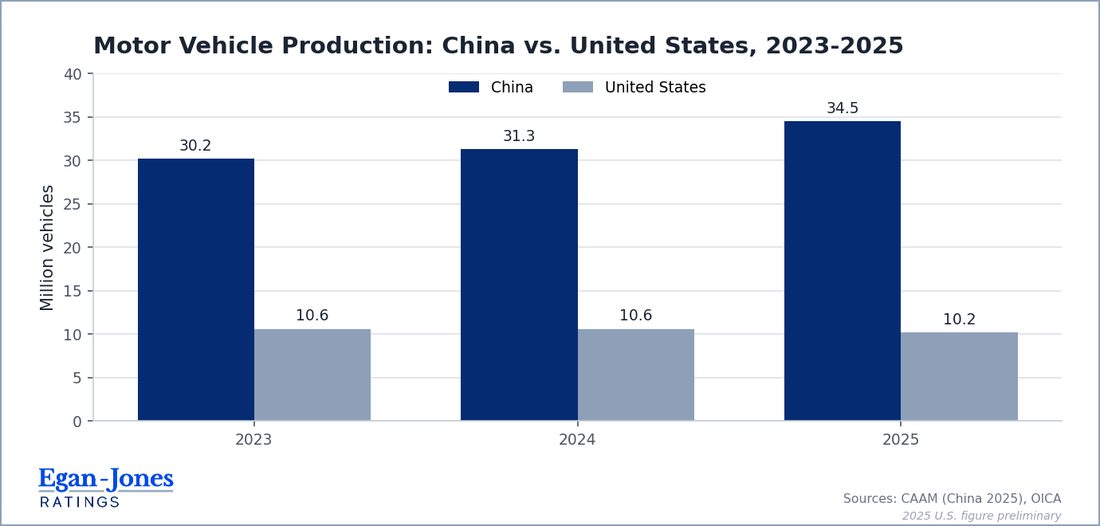

The Chinese automakers have come to dominate world trade (see Appendix B), and it has only been US barriers which have kept them at bay in this country. Given the current administration's focus on job creation, our bet is that we will soon see some plants being erected in the US, following the path of the Japanese manufacturers in the 1970s and 1980s.

It has been decades since domestic steel manufacturers were deemed to be on the cutting edge, and recent developments suggest that some Chinese firms have developed better products (see Appendix C).

China has been and continues to be a leading provider of drone parts and other electronic products.

The winners are likely to be American job seekers (from the new factories to be established) and those firms which gain increased access to the Chinese markets. For a list of those firms, a good starting point is probably those executives who were included in the trip with the president:

The world is changing rapidly. This installment aims to provide a framework of possible major shifts for the benefit of sophisticated institutional investors and risk managers.

Vehicle production

Chinese automakers have rapidly expanded output, widening their lead over US production.

Rather than a single “superior steel,” the strongest evidence points to several advanced, high-performance steels where Chinese producers have set world records or broken long-standing foreign monopolies. The marquee example is ultra-thin precision stainless steel foil, nicknamed “hand-tearable steel,” alongside rare-earth-treated specialty steels and a broad shift from commodity rebar toward high-value-added grades.

Developed by Taiyuan Iron & Steel Group (TISCO) in Shanxi Province, this is a wide precision stainless steel foil “as thin as the wing of a cicada.” TISCO produced a 0.02 mm-thick, 600 mm-wide foil in 2018, then set a world record in 2020 at just 0.015 mm thick while keeping the 600 mm width, less than a quarter the thickness of A4 paper and thin enough to tear by hand. Because it is so valuable, it is sold by the gram rather than by the metric ton. The technology had long been monopolized by a small number of developed countries (notably Japan and Germany). The flexible foil can reportedly be folded up to 200,000 times without losing shape, with applications in aerospace, precision instruments, foldable-screen 5G electronics, and new-energy batteries.

Baogang (Baotou Steel) reported a rare-earth refining innovation aimed at specialty steel grades, targeting automotive steel needing enhanced formability and strength, offshore wind-turbine plate, and marine-engineering applications, segments where superior steel properties command premium pricing.

China's steel sector has moved from commodity products toward high-tech, high-value grades. By end-2025, an industry institute reported that 16 Chinese steel enterprises had approached or attained world-class standards, and in 2025 Xinsteel Group won export orders of over a thousand tons of high-end wear-resistant steel plate into North America and Southeast Asia. Leaders like Baosteel and Shougang now supply advanced high-strength steel for car bodies, aerospace, and high-speed-rail car bodies. The China advanced / ultra-high-strength steel market is projected to grow from about $72.4B (2025) to $123.8B (2032).

Important nuance. The evidence supports that Chinese manufacturers have developed world-leading products in specific niches, most clearly the world's thinnest hand-tearable steel foil, and are rapidly advancing in advanced high-strength and specialty steels. It does not establish that Chinese steel is broadly “superior” across all categories; much of China's output remains commodity-grade, and several cited sources are Chinese state or industry outlets. The accurate claim is leadership in particular high-end products and a fast climb up the value chain.

1. President Trump's China trip and attendees - BBC News, bbc.com.

2. Thucydides Trap case file - Belfer Center for Science and International Affairs, Harvard Kennedy School.

3. China exports-to-imports ratio - OECD, via FRED. Chinese yuan / USD spot rate - Board of Governors of the Federal Reserve System, via FRED. Vehicle output - CAAM (China 2025) and OICA (2023-2024).

Appendix C - TISCO hand-tearable steel (0.02 mm foil, sold by the gram; folds 200,000 times) - Qiushi, Nov 2020.

Appendix C - 2018 0.02 mm and 2020 world-record 0.015 mm / 600 mm foil; foreign monopoly; applications - Xinhua via Newsflare, Aug 2024.

Appendix C - 2023 0.015 mm world record on domestically produced equipment - report citing Tsingtuo Group, Nov 2023.

Appendix C - Technical baseline (Japan/US firms at 0.05 mm, width <450 mm) - Chinese patent application, Justia.

Appendix C - Baogang rare-earth refining breakthrough for specialty steel - Discovery Alert, Nov 2025.

Appendix C - Shift to high-end steel; 16 enterprises near world-class; Xinsteel exports - SunSirs, 2026.

Appendix C - Baosteel / Shougang advanced high-strength steel for autos, aerospace, rail - industry blog, Nov 2025.

Appendix C - China advanced / ultra-high-strength steel market $72.4B (2025) to $123.8B (2032) - Mobility Foresights, Mar 2026.