.svg)

The following episode from the life of Socrates has been told countless times and goes as follows. One day, as a famous Sophist¹ was returning to Athens from a lecture tour in Asia Minor, he accidentally ran into Socrates on the street, which is where the great philosopher spent most of his waking hours, posing the same question to various people, in this case to a cobbler about what a shoe is.

Sophist: My dear Socrates, are you still sitting there saying the same thing about the same thing?

Socrates: Yes sir, that I am. But you, who are so very smart, you never say the same thing about the same thing!

Many of you already know me and therefore can easily guess what I’m going to say, for I too only have one thing to say about structured securities, namely the same thing. Be warned, though, because reading this may bore you to tears. Although there’s fatigue risk, I beg your indulgence one last time, for despite its simplicity and self-evidence, indeed perhaps because of it, what I’m about to say appears to be the most complicated no-brainer on the Street, and it is this: credit risk in structured finance is fundamentally different from that in corporate finance.

Whereas corporate ratings are static by definition, structured ratings are essentially dynamic, also by definition. Yet, both are treated identically by the vast majority of investors, traders and rating agencies. At least, until now. The consequences that follow logically from this essential difference can neither be circumvented nor avoided. Of course, they can always be ignored, and commonly are, albeit at the investor’s own expense.

The entire basis of corporate security valuation and thus, rating, is the so-called “going concern” assumption underlying accounting theory, which assumption also gives its practitioners license to do, or not to do, all kinds of things in the name of continuity and stability. In a nutshell, corporations are like diamonds and true love, i.e., they are forever. This factotum naturally gives rise to the basic metric of corporate credit risk: bankruptcy, i.e., the death of an entity that is never supposed to die. Therefore, the probability of bankruptcy is the proper measure of corporate credit quality.

By contrast, structured securities are issued out of English trusts with lifetimes capped at “a life in being plus 21 years²”, clearly not a fixed number but now approximately a century. In practice, structured securities are usually backed by static pools of financial assets³ that, unlike corporations, do amortize secularly within a timespan much shorter than 100 years. For instance, consider a garden-variety auto ABS deal whereby any loan in the pool has an initial, remaining maturity of 72 months or less. As a result, it is tautological and trivial to say that within 6 years or so, the pool balance will drop to zero owing to the initially unknown dynamics of scheduled principal amortization, prepayments and defaults. Since credit risk is risk of principal loss, the dynamics of default form the crux of structured security rating, valuation and analysis.

Conversely, six years from now, Microsoft will be no closer to maturity than it is today, not to mention that a corporation is not anything like a static pool of financial assets. In other words, a corporation always lives “in the present”, whereas structured securities are essentially temporal. Like human beings, their future must be analyzed from their past.

The upshot of such rather basic considerations regarding linear time is that structured securities exhibit the kind of credit-risk optionality, and thus distributional convergence, that does not exist in corporate finance. Once the pool begins to reveal itself via periodic trustee reports, not only does this new information allow the analyst to update the initial rating and/or valuation at the same frequency, but the remaining time for additional defaults to take place is also being compressed. This is something that does not happen in corporate finance.

In the neighborhood of the 72-month pool maturity, it is a foregone conclusion that an analyst is in a position to know the credit quality of any outstanding securities in the pool with 100% certainty owing to the obvious fact that, to all intents and purposes, the probability density function of remaining defaults has been reduced to a Dirac delta-function from a combination of deleveraging an optionality. What is not obvious to the naked eye is that even within two or three years post-closing, the fate of the securities backed by the pool will start coalescing towards quasi-certainty, and that their rating will start moving up towards AAA.

In passing, this phenomenon is also true of market risk in general. The remaining variance at current time of a Wiener process with local standard deviation and maturity is known to be σ²(T — t). In that case as well, once remaining deal-time converges to zero, the remaining distribution of possible outcomes becomes “singular”. By definition, remaining variance must be zero at the trust’s legal final maturity date.

Note that the foregoing analogy with market risk was inserted merely for the sake of academic exposition. This is because market risk is symmetric, but credit risk is stochastic in the original Aristotelian sense of that word. Although one could always argue that the price of any common stock can theoretically move up or down with 50% probability on each side owing to the “efficient” market hypothesis, this does not obtain in credit risk, because no obligor may “un-default”. A true stochastic process is asymmetric the way it is in an American courtroom in which a “not guilty” verdict is not the logical opposite of “guilty”, which is obviously “innocent”. In American law, no one is innocent.

The inescapable upshot of these fairly self-evident considerations is also self-evident, which is that, as deals mature or season, structured-security ratings can move either up or down, but they cannot remain the same for very long after issuance. Once trustee reports come in, and the cumulative default-percentage⁴ expected at origination materializes, doesn’t, or is in fact exceeded, the renormalization process already alluded to will perforce cause ratings to become dynamic as well.

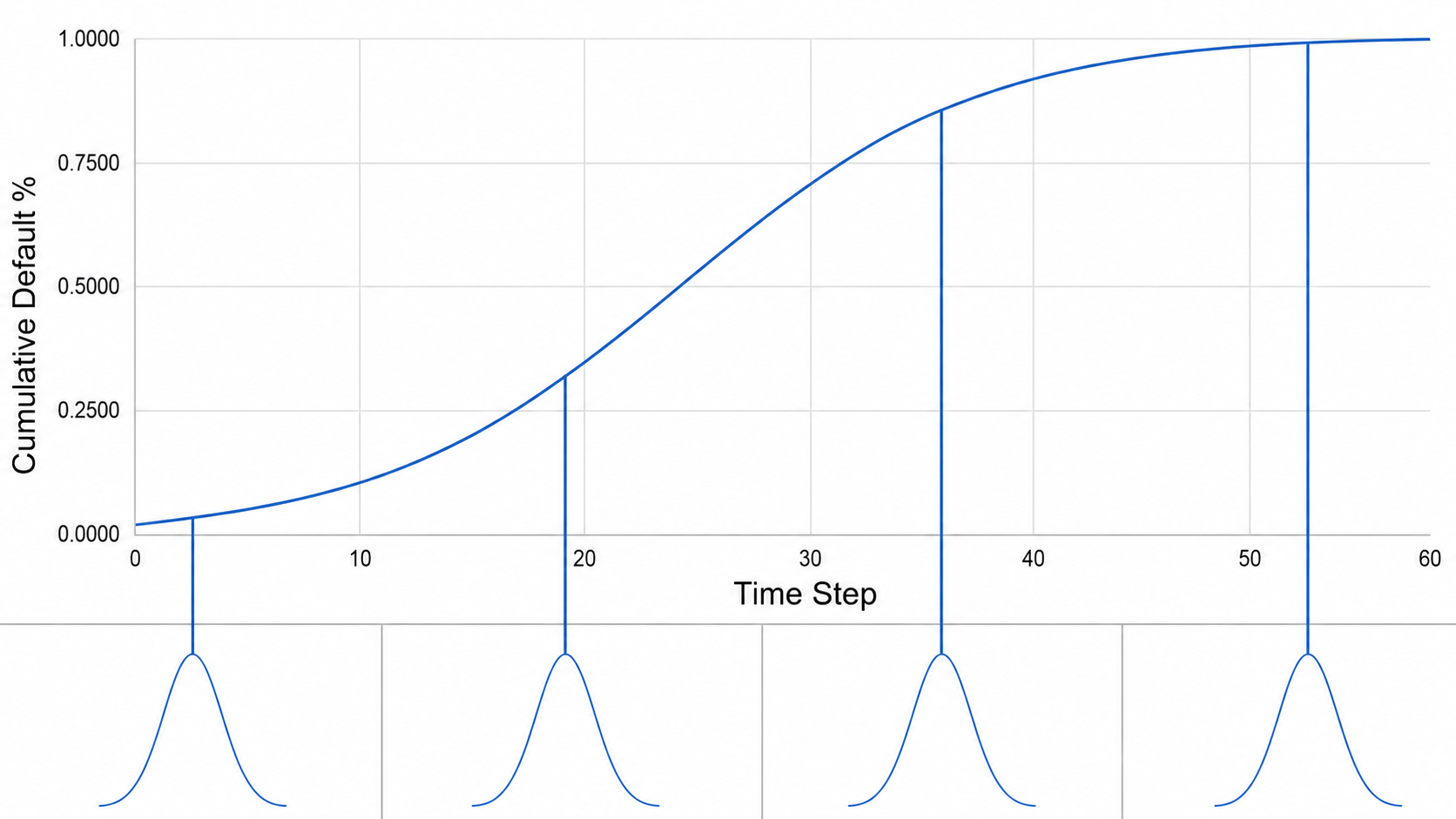

Yet, probably due to a priori corporate bias, most structured investors and rating analysts regard the unfolding situation as depicted in Figure 1. When defaults are realized and cumulate on their way to some TBD, asymptotic level, investors insist on maintaining the standard deviation of the remaining-default distribution at its original value, which keeps the rating unchanged across time (ignoring normal deleveraging for now).

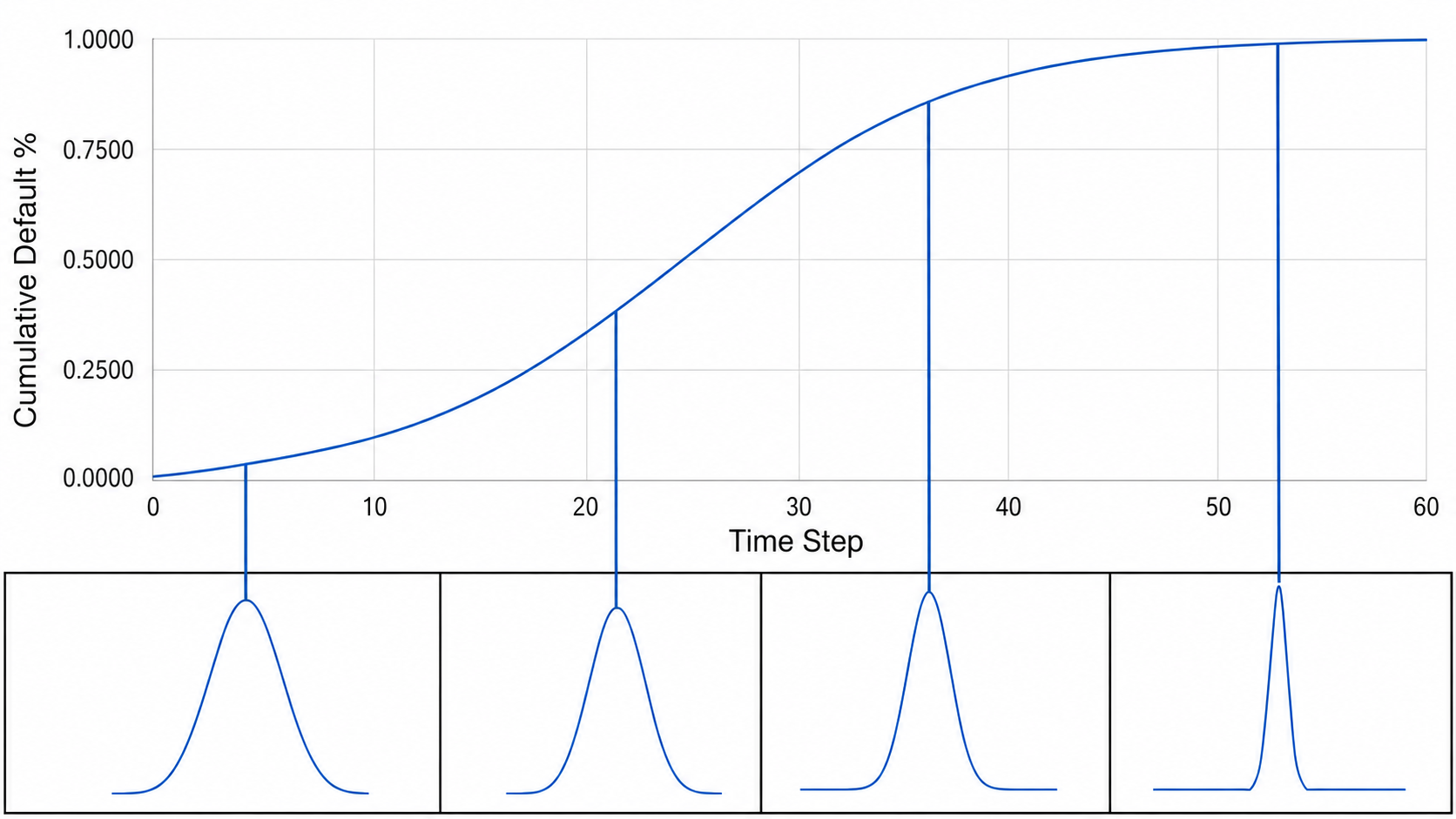

Consequently, ratings are never allowed to exhibit their dynamic nature the way they ought to be, i.e., to move up or down naturally without any special event taking place. In keeping with our logic, rather than the erroneous structured credit paradigm in Figure 1, what actually happens is shown in Figure 2. There, we have explicitly recognized the convergence of the standard deviation of remaining defaults towards zero as the unfolding default-history transforms the relatively large uncertainty at closing into absolute tranche-wise certainty due to the intrinsic, and therefore, unavoidable outgrowth of the pool’s monotonic amortization dynamics.

With respect to structured transactions performing approximately as expected, this means that the rating of all securities in the trust will eventually telescope to AAA, although the rating of junior tranches will clearly end up there later than that of more senior tranches, i.e., senior securities already AAA at inception have nowhere to go. By contrast, subordinated bonds will usually traverse the entire credit spectrum from their initial credit rating to AAA, thus offering lucrative trading opportunities to investors and secondary Street traders alike.

The identical process will, of course, unfold vis-à-vis “bad” deals. In that case too, the probability that credit losses will eventually be experienced with respect to one or more tranches will converge to 100%. Therefore, here too valuation uncertainty telescopes to zero. In other words, in structured finance valuation, hence rating, uncertainty eventually drops to zero within all transactions. The fact that some investor or other is guaranteed to lose money on her investment is not a sign of “risk”, because risk is only volatility, i.e., uncertainty.

It is regrettable that many investors are still confused between the mean and the standard deviation. Even the greatest risk manager is only able to reduce the standard deviation of the timewise loss distribution to zero, not its mean value, since that would imply that risk itself has been eliminated, which is impossible. Risk is like mass, momentum and energy; it is conserved. If you don’t have it, someone else does. As Warren Buffett is fond of saying, investors who don’t know that risk is conserved usually end up bearing all of it.

If you’ve been paying attention, dear reader, by now you should have realized that there’s a very high likelihood that the rating of the structured securities you now hold is all wrong.

If you’ve never heard of the foregoing and are still comfortable with static ratings in structured finance, you’re leaving a lot of cash on the table, because it is a virtual certainty that most of the deals you bought are good, not bad ones. Therefore, the credit rating of the majority of your assets is understated, sometimes by a lot depending on seasoning. Likewise, the discrepancy between the actual fair market value of your assets and their book value given their original, presumably static rating increases monotonically with every passing day. In addition, the larger your portfolio, the more serious and expensive the situation becomes for your firm, and therefore, for you. As Clint Eastwood once said, “dyin’ ain’t much of a living, boy!”

Since your firm holds risk-capital commensurate with credit risk, it also means that you probably hold too much capital covering non-existent credit risk. In many cases, a tranche now par-valued could easily be re-marked to 110% and more. Doing this rationally could then enable your department either to free up precious balance sheet capital, or else allow the trading desk to make a sizable profit, simultaneously compensating your firm for having the analytical depth, and the guts, to assume the original credit risk.

As things now stand, neither the investor nor the obligor is benefiting from the secular rating dynamics that prevail in structured finance, which in most cases is skewed towards improving credit quality.

It is a foregone conclusion that no investor would ever accept coupon-reduction in recognition of reduced credit risk, so let’s not go there. On the other hand, as an investor you have the power to turn this whole thing around and increase portfolio yield by capturing credit optionality for yourself, instead of holding needless risk capital basically at SOFR flat. And if you behaved as suggested, you would likely have more cash in reserve to come to the rescue of the relatively few deals you invested in that do end up heading South.

The choice is yours and yours alone.

✉ For more information, contact Sylvain Raynes at sylvain.raynes@egan-jones.com

Sylvain Raynes' main area of expertise is structured finance. For the past thirty-five years, he has been involved in various aspects of structured financial analysis involving a wide array of asset classes.

Beginning at Citicorp, he was responsible for the design of the Consumer Bank’s credit card loss and recovery model. At Goldman, Sachs & Co., under Fischer Black’s supervision, he was part of a team involved in the modeling of derivative products and in many other credit-based initiatives. Later, while a senior analyst at Moody's Investors Service, he continued to focus on the credit aspects of exotic assets such as structured settlements, aircraft ABS and insurance premiums while adding legal and bankruptcy analysis to his toolkit. He helped structure new financial instruments and developed the methods now used by Moody’s to rate tax liens, aircraft leases, railcar leases, car rental receipts, structured settlements, tax liens, default-receivables, and charge-card receivables securitizations. At Credit Suisse First Boston and Paine Webber, he developed the analytical method used to value securities issued pursuant to cash flow CLOs, aircraft-leasing and medical receivables transactions.

Dr. Raynes holds a Masters’ and a Ph.D. in Mechanical & Aerospace Engineering from Princeton University and a Diploma in numerical analysis from the von Karman Institute in Brussels, Belgium.