.svg)

On June 9, Anthropic released Claude Fable 5, its most capable model to date. Three days later the US government issued an export-control directive, and Anthropic disabled Fable 5 and its sibling Mythos 5 for every customer worldwide.1 Access was restored on July 1, after the Commerce Department lifted the controls.2 During the blackout, Z.AI released GLM-5.2, an open model that ranks just behind the Western leaders at a fraction of the cost.3 A coach whose play just worked sends the offense back to run it again. China is doing much the same in AI, and this installment offers sophisticated institutional investors and risk managers a framework for the shift and what it means for credit.

The Chinese open models (GLM-5.2, DeepSeek, MiniMax) sit at the left, near the frontier on capability and far below it on cost. Cost per task is an estimate; dot color reflects output speed.34

China has been the world's most effective second mover, building at scale what others design first. AI is likely to follow, because it has come to resemble a manufacturing business. Training and running frontier models takes vast capital, land, and power, and Beijing has spent years making the country good at exactly that. The same build is harder in the United States, where permitting, zoning, and other legal hurdles slow the physical work, a burden that grows with a country's wealth.

GLM-5.2 is free to download and change, it performs close to the best Western models, and it costs far less to run. A task that runs a few dollars on Claude Opus 4.8 or GPT-5.5 costs cents on GLM-5.2, and it plugs straight into the tools US developers already use.35 Its lineage is not fully its own. GLM models sometimes identify themselves as Claude, and OpenAI has accused Chinese developers of training on its models' output; the rules on such copying are unsettled across the industry.6 The model landed about six months behind the comparable Western release, a gap that has held for more than a year.7

Impact: OpenAI and Anthropic sell intelligence by the token, and a free model at a tenth of the price undercuts that. High-volume, well-defined work, such as customer support, code completion, and bulk document processing, leaves first, squeezing API margins.

Beijing runs AI the way it ran manufacturing: an industry to plan, fund, and keep at home. Manus is the clearest case. The startup, founded in Wuhan, moved to Singapore in 2025 and agreed to sell to Meta for about $2 billion that December.8 China killed the deal. In April its planning agency ordered the sale unwound on national-security grounds, and by June Meta had cut Manus off to comply, the first reversal of a completed cross-border AI acquisition.8 New rules effective this month let Beijing do it again and block transfers of talent in sensitive fields, and firms like Moonshot and MiniMax are being pushed toward Hong Kong and domestic money.9

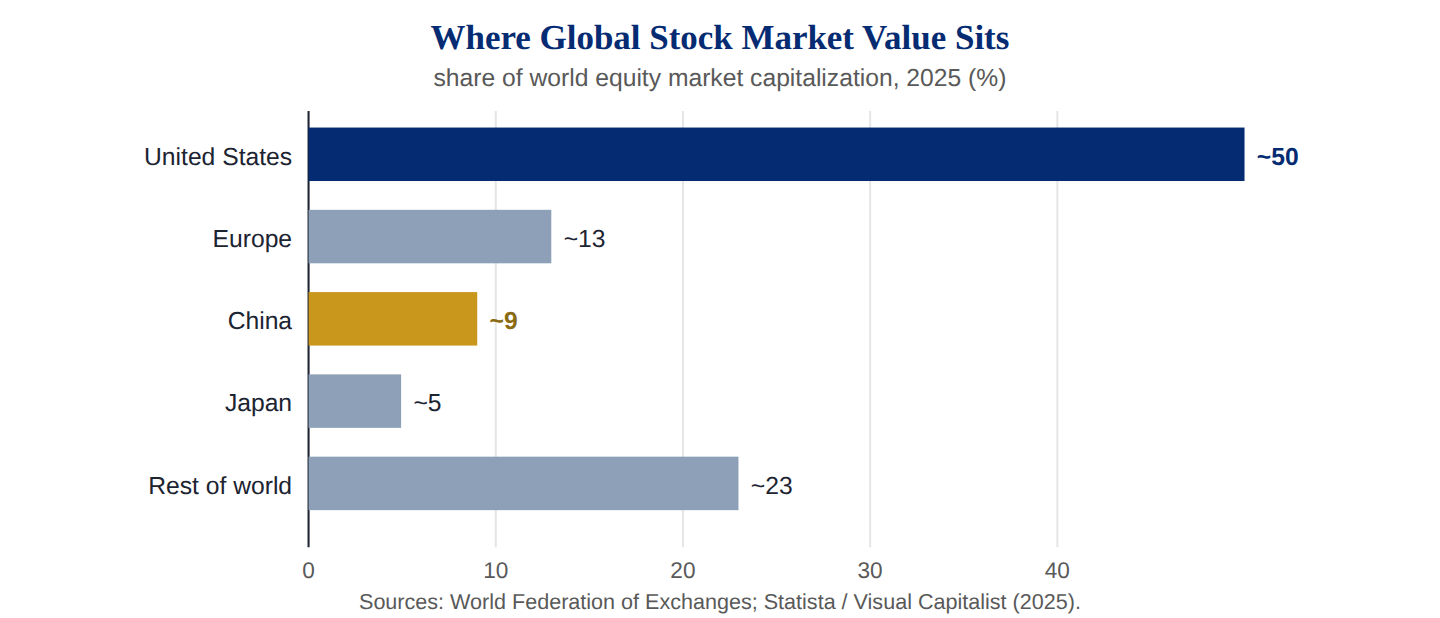

This makes China harder for outsiders to own. US and Chinese equities have diverged for years, and the United States now holds about half of world market value against roughly a tenth for China.15

US-listed companies are about half of world equity value, roughly six times China's. For a global investor, China is a small slice of what can be owned.

Impact: A US fund has almost no clean way to own the upside of Chinese AI, now that Meta's Manus purchase is unwound and MiniMax and Moonshot are steered to Hong Kong. Money that wants AI exposure stays in Nvidia, Microsoft, and the other US names by default.

AI now behaves like heavy industry. The four largest US technology companies plan to spend about $725 billion on capital projects in 2026, most of it on data centers, chips, and power, and their capital spending runs near half of revenue.10 The inputs are physical and slow to build: advanced chips, memory, cooling, and above all electricity.

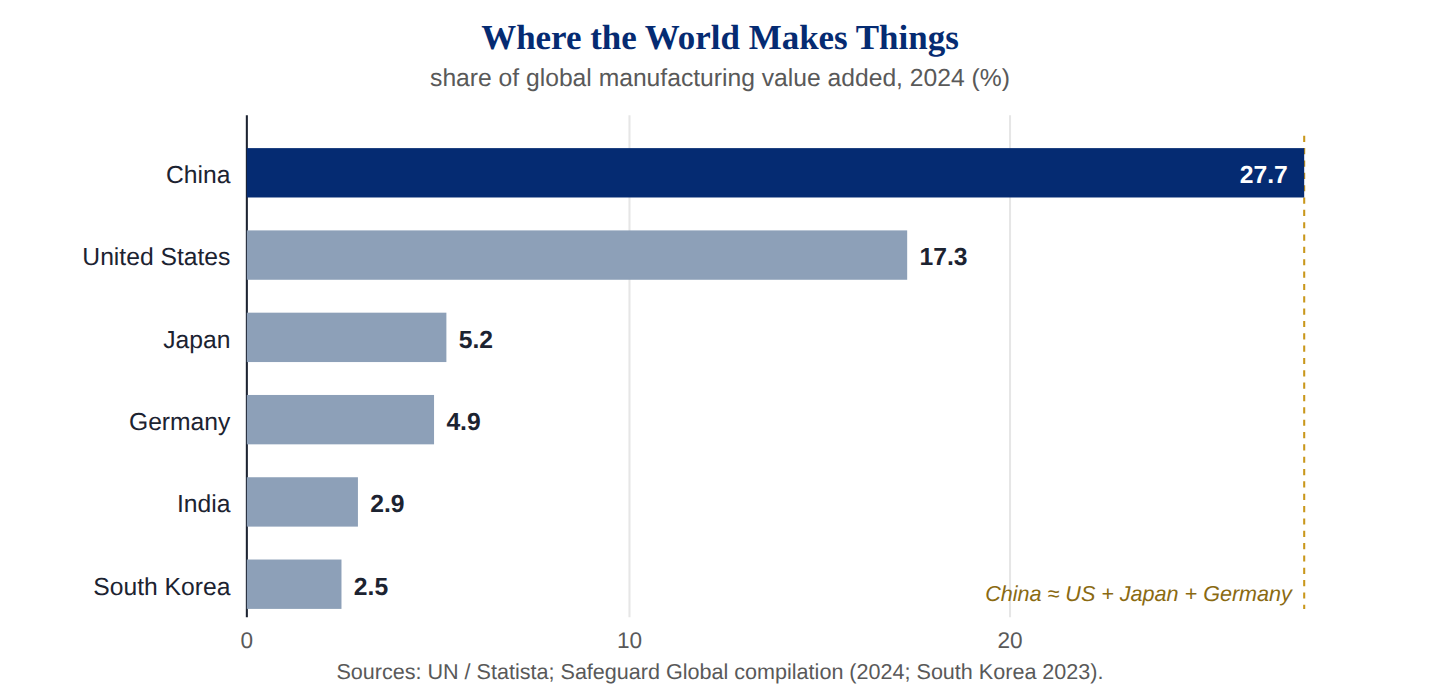

China holds the edge in all of them. It makes more than a quarter of the world's manufactured goods by value, about as much as the United States, Japan, and Germany combined.11

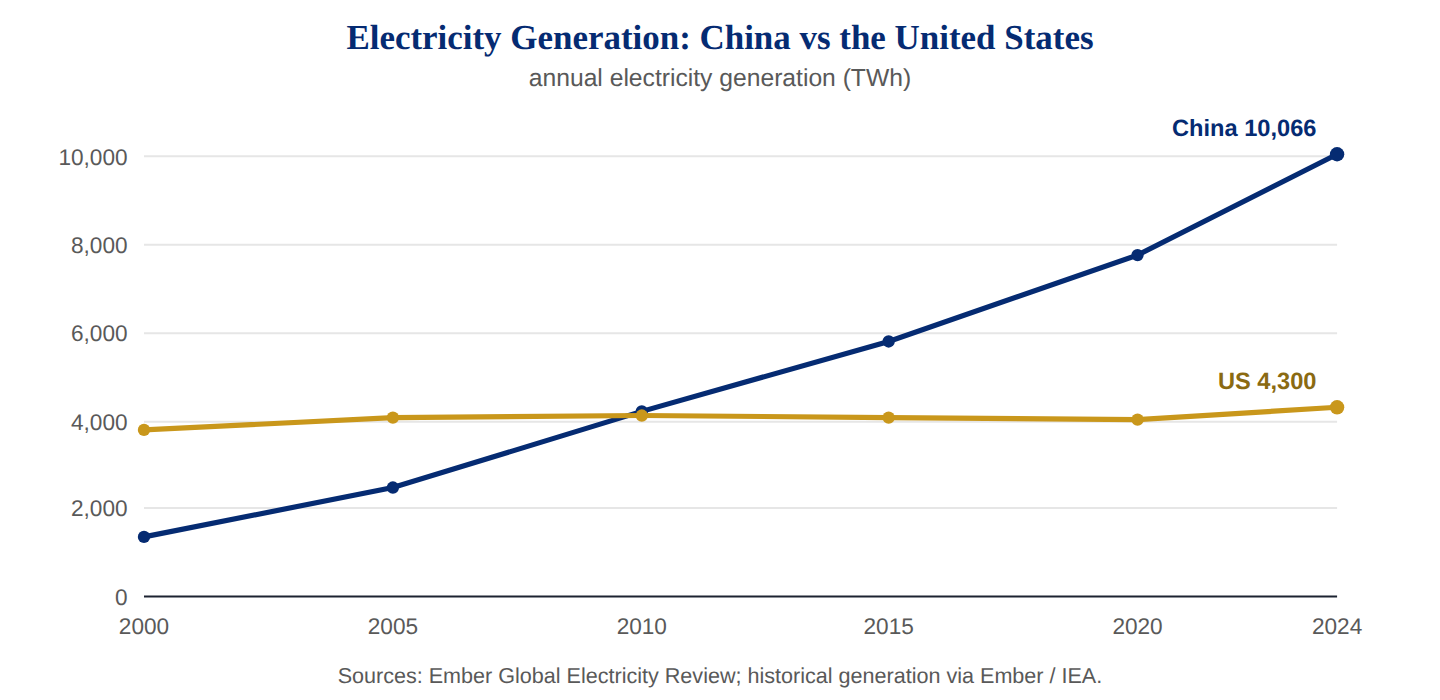

The bigger gap is power, often a limiting factor for any new data center. China's generation has grown sevenfold since 2000, passed the United States around 2011, and now runs more than double it. US output has been flat for two decades and is only now rising as data centers pull on the grid.12

The Chinese state sets electricity prices and pays to build new capacity, and power there costs about half what it does in the United States.13 The same build in the United States runs into permitting, grid-interconnection queues, and litigation. Western Europe is the extreme case: high costs and slow approvals have left it without a single frontier AI company or hyperscaler, much as it sat out mobile and software industries. Its strength is in components, like ASML's machines and Arm's chip designs, while the platforms get built elsewhere.

Impact: Microsoft, Amazon, Google, and Meta can buy chips faster than the US grid can power them, and interconnection queues and local permitting now gate their data centers. The binding constraint is electricity, which favors builders who are not tied to the US grid.

AI becomes more useful when it runs a machine. A model that can drive a car, work a warehouse, or steer a robot does what a chatbot cannot. Much of that hardware is already Chinese: robot vacuums, robotic lawn mowers, and more than half of the world's new industrial robots, all built in or shipped from China.14

The same machines can be used for spying and for war. Robots, phones, and computers already are, and AI models will follow. Western software has done this before: the Stuxnet worm was used to cripple Iran's nuclear centrifuges. A country that lets a rival build its machines depends on that rival; hence, so owning the hardware matters.

Impact: The value in AI is shifting toward the hardware, and in consumer hardware the United States has already lost the lead: RCA and Zenith televisions gave way to TCL and Hisense, IBM's PC line became Lenovo, and GE Appliances now belongs to Haier. China has not captured much of the profit, though. Overcapacity and years of price wars have driven factory prices down and crushed margins, so the benefit has flowed to consumers, many of them abroad, while investors have earned thin returns.16

The reality is that AI firms are not only competing among the current leaders, but emerging firms which are following the paradigm of “faster, better, cheaper”. Adding to the mix is the physical world of robots and such, which promises major changes in this rapidly developing field.

The category-defining work in AI is being done in the United States, while the capacity to build, power, and embody it at scale sits increasingly in China.