.svg)

Recently, xAI and SpaceX merged, suggesting the possibility that Mr. Musk is planning on building future data centers in space. Such a development, if feasible, might significantly reduce electricity and cooling costs, as space is naturally cold, and solar cells would provide the electricity.

The rub is whether the launch and maintenance costs would offset the savings in electricity and cooling. Unless our calculations are materially off, the launch/lifting costs at present make the project unfeasible. Given the fact that Mr. Musk is highly intelligent and assuming our analysis is directionally correct, what could possibly be the reason? For this, see our conclusion.

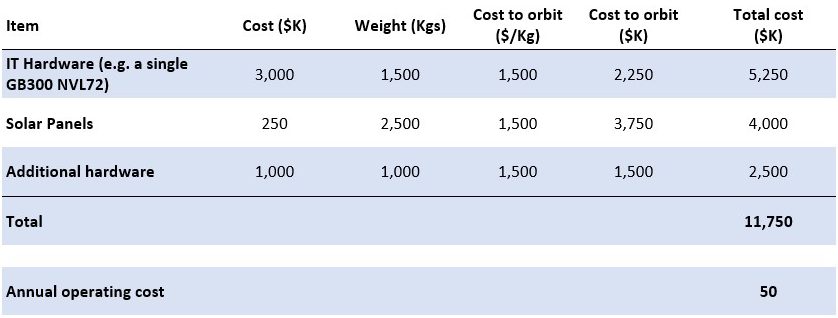

The dream of “data centers in space” is driven by the potentially lower operating costs off Earth. Comparing unit economics makes the problem clear. Of course, there are economies of scale for both Earth and Orbit cases.

According to Figure I, we assume the upfront cost of a single data rack (e.g. GB300 NVL72) on Earth is roughly $3,260K, with $250K in annual operating costs. Assuming (i) each rack weighs 3,000 pounds or 1,500 kg1, and (ii) the cost to send 1 kg to orbit is $1,500 per kg, then (iii) the lifting would cost nearly $12,000K, which would trump any annual savings on electricity, particularly since the racks are expected to be obsolete within seven years.

Thus, assumptions about technological development are critical. The only way that space-based data centers appear workable in the near future is: (1) vastly reduced transportation costs - roughly 15x, (2) longer lifecycles for hardware, (3) lighter hardware, or (4) increased operating costs on the ground.

Conversely, should lower transportation costs fail to manifest, operating costs from energy and water decline, or hardware costs decline, the dream of “data centers in space” at scale is likely to remain exactly that.

Note, we are setting aside the issue of whether the heavy demand for data centers will remain. On this score, for the most part, it is the obligation of low or no net debt, high market cap stalwarts (e.g., Meta, Alphabet, Microsoft, and Oracle) to afford these obligations.

Turning to the recent rout in the valuations of SAAS firms, it has been dramatic and ugly.

Salesforce (NYSE:CRM) experienced a 34% decline over the past year, falling from $293 to $192. The concern is that artificial intelligence will reduce the value of seat-based SAAS firms as alternatives can be made cheaply.

Further, there may be a reduction in demand for many SAAS products as those tasks are replaced by automation. Relevant to CRM, the replacement of salespeople by new technology has occurred slowly over decades and is well depicted in the plays “Death of a Salesman” and “Glengarry Glen Ross.”

While it is clear that AI will facilitate programming, the switching costs and hassle remain. There is little doubt that Salesforce is expensive on an absolute basis. The larger concern for many sales managers is the effectiveness of their sales teams; a marginal improvement translates into major gains.

Additionally, there is the challenge of accessing the market. Even if a far better product is developed at minimal cost, it is difficult to reach and convert the buyers. Perhaps the most likely scenario is that one of the related incumbents offers a more compelling product. The firms that come to mind are Microsoft and Alphabet (to a lesser extent), both of which are already embedded in the workflows of many workers. However, Microsoft already offers Office 365, which has a CRM component, and it is a distant competitor.

The premise behind many SAAS investments is that once market position is developed, the customer base is sticky, and that marketing and development costs can be reduced if needed to service debt. Nonetheless, there is little doubt that the technology tools that are being developed will change the industry.

The challenge in being a sophisticated institutional investor and risk manager is sorting through the noise to determine the true conditions in the market. For the time being, it appears that space-based data centers make little sense. Regarding Mr. Musk’s motivations for the move, the short answer is that we do not know, but perhaps that old adage is a possibility: “It is always about the money.”

Competitors OpenAI and Anthropic have similar record-breaking IPOs planned, and it appears Mr. Musk’s goal is to front-run them getting to market.

It is probably easier to provide funding for xAI and other ventures via the proven winner of SpaceX. A similar move was made in 2016 via Tesla’s acquisition of SolarCity as the combination eased SolarCity’s cash crunch. Being a leading entrepreneur is more than just developing terrific businesses; it also involves figuring out ways to fund those businesses.