.svg)

The results of Jack in the Box’s 2026 annual meeting suggest that shareholders are expressing concerns about sustained underperformance and board oversight. Director support levels were materially below market norms following a period of declining financial performance and share price erosion.

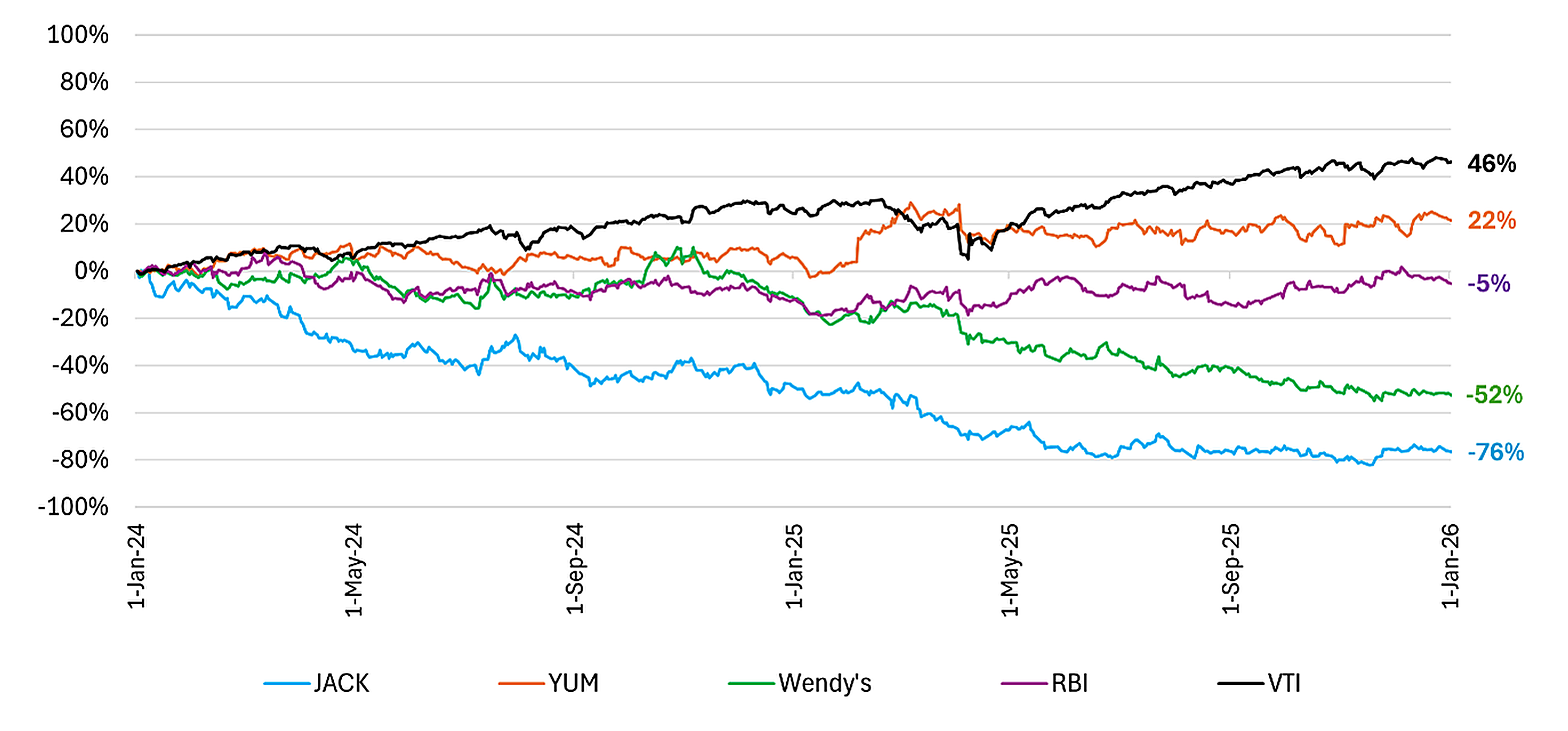

Recent company performance provides important context for voting outcomes.

Jack in the Box’s most recent financial results were weaker than expected.

For the fiscal quarter reported on February 18, 2026, the company reported earnings per share of $1.00 versus expectations of $1.10 and revenue of $349.5 million compared with $355.7 million expected. Additionally, same-store sales continued to decline 6.7% year-over-year for the first quarter of FY 2026.

The market reaction was immediate. Shares declined approximately 18% on February 19 and a further ~7% on February 20. Over the past two years, Jack in the Box has lost approximately 80% of its value.

Against this backdrop of sustained underperformance, Egan-Jones recommended withholding votes from several directors, including the chairman.

Another proxy advisory firm recommended support for all ten directors. In their report, the firm acknowledged that “the company’s TSR has been negative and underperformed across all measurement periods” and that “performance during Goebel’s tenure has been disappointing,” but concluded that support for all management nominees was warranted.

Shareholders delivered their verdict at the company’s annual meeting on February 27.

Chairman David Goebel was reelected with just 50.5% support. Several other directors, including Guillermo Diaz Jr., Vivien Yeung, James Myers, and Madeleine Kleiner, received approximately 80% support, a support level that is materially below the roughly 95% support typically observed at Russell 3000 companies.

Directors whom Egan-Jones recommended against received significantly less shareholder support, which suggests that investors shared our concerns about performance and management oversight.

Egan-Jones is the only major independent proxy advisory firm and does not receive consulting revenue from issuers. This structure helps avoid potential conflicts that can arise when advisory firms maintain paid relationships with the companies they evaluate.

Our analytical framework places significant emphasis on long-term total shareholder returns and relative performance versus peers when evaluating director elections. Sustained underperformance is therefore a central factor in our analysis, both in contested situations such as this one and in routine director elections.

Institutional investors are ultimately evaluated based on portfolio returns. Our approach is designed to support that objective by linking vote recommendations to company performance.

If you would like to discuss our approach, we welcome the conversation. You can book a time with us here: https://ejproxy.com/book.