.svg)

All businesses operate in a broader environment, the political environment. Periodically, that environment shifts massively with dramatic and widespread effects.

This theme, while hopefully rare, can be devastating for sophisticated institutional investors and risk managers. A way of thinking about this installment is the collision of politically popular public policy and sound economics.

The unwritten rule for proper taxation is to extract some money, but not too much so as to kill the taxpayer. For New York City residential landlords, the policies pursued by the city might feel as though the objective is to drive them out of business.

In fact, with the inauguration of the new mayor in New York, a self-professed socialist, it appears to be exactly the policy. On the revenue side, the allowed rents remain below levels needed for proper maintenance of the buildings, while fines are levied for exactly that: not maintaining the buildings. Perhaps adding insult to injury, the new mayoral administration wants the city government to have a preferred position in bidding for any properties. The likely rallying cry of landlords is that we cannot pay for repairs, we are fined for not making repairs, and now you want to steal the buildings via purchases at low-ball prices. A WSJ article documented the dilemma.

Commentary: Perhaps some solace can be obtained by suing the city, but the likely jurisdiction for the cases is probably the courts of the very city they are fighting.

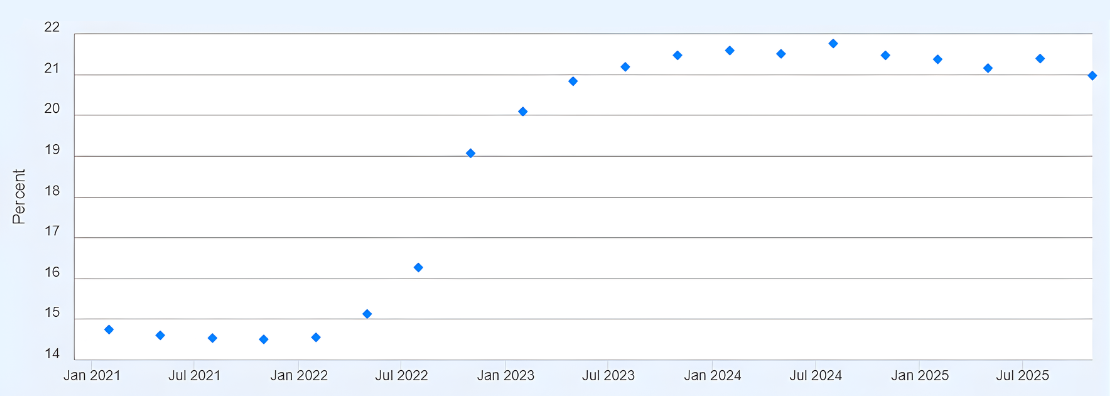

The current administration claimed that credit card interest rates should be capped at 10%, a level approximately half of the current rate:

Presumably the impetus for the policy is an attempt to benefit the roughly 100 million Americans who hold credit card debt at an average balance of $6,501 per person. To the borrower, it has a broadly similar effect to Biden’s student loan moratorium. Perhaps more importantly, lowered cost of debt will incentivize greater indebtedness and provide a short-term jolt to the economy and increase the likelihood that the incumbents perform well in the midterm election cycle.

Banking executives may seek to convince the administration that it is uneconomic to maintain many current customers at half the current rate and if they fail, will become more restrictive in their lending practices. The first task appears daunting, and the second is likely to be difficult from a public relations perspective.

Commentary: The current administration in Washington has a history of taking drastic stances and reversing them.

For the past several decades, major energy companies have seen little progress in their claims against the Venezuelan government for the government’s nationalization of assets. Considering Nicholas Maduro was removed as president, the probability of realizing some return becomes more realistic, as does the possibility that the business environment in the country improves.

Commentary: The sovereign gives, and the sovereign takes. Time will tell whether the environment will materially improve.

As of 2021 and early 2022, 30-year mortgage rates were at rock bottom levels of 3.0% and a bit less. The “largesse” was the result of the central bankers buying securities in an effort to stoke the economy. In contrast, current rates on 30-year mortgages are in the area of 6.0%. For those fortunate or smart enough to lock in the low rates, the liability is essentially an asset as their funding cost is far less than current rates. However, on the flip side, the prevalence of low-rate mortgages creates a disincentive for moving, thereby causing constipation in the housing market; empty nesters should be moving to smaller homes, but in many cases are not because of low locked-in rates.

Commentary: Governments often are not responsive to the longer-term consequences of their actions.

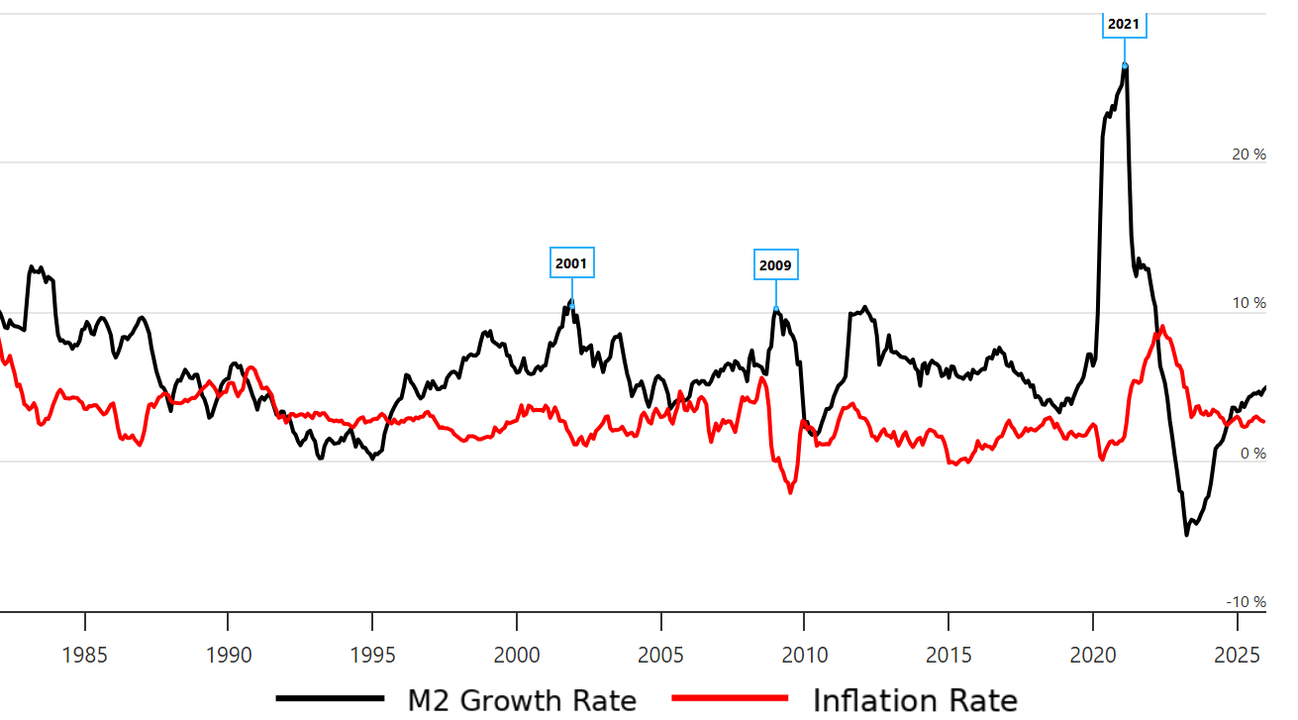

At the Bretton Woods Conference in 1944, it was decided that the American dollar would become the world’s reserve currency and remain convertible to gold. When the dollar officially became independent of gold in 1971, its status as a reserve currency and medium of exchange remained. The benefits to the American economy were tremendous. There has been a broad and deep market for American debt and currency. Thus, debt has been cheap, and additional dollars have been in high demand globally, meaning inflation is lower than it would have been otherwise given America’s monetary policy.

The recent increase in gold prices likely indicates some skepticism of the future supremacy of the dollar and may indicate pressure on the global demand for dollars or American debt. Notably, trade deals are increasingly being made in currencies other than the dollar. This transition has occurred in part to avoid American sanctions.

Of course, gold is cumbersome to trade, though this can be largely offset by using deposits with a trusted third-party custodian (once the United States Federal Reserve).

Historically, banks had a lock on savings and checking accounts. Because of this situation, the banks had the support of the federal government via an FDIC guarantee of deposits (i.e., liabilities) but also some regulation. While money market funds provide some competition, in reality, because of various limitations, they are not serious alternatives to checking accounts. Perhaps with the emergence of stable-dollar cryptocurrencies and rapid settlement periods, the landscape is changing.

Commentary: The hype around cryptocurrencies has been stunning, but it will take time for broad acceptance.

We focused on this topic because, with the tremendous power of the state, the environment can change rapidly with widespread and long-lasting effects.