.svg)

Overview

Over the past couple of years, massive amounts of capital have been devoted to data centers. A natural question is whether the expended capital is soundly placed and whether investors can expect a reasonable return. From the typical data center creditor’s perspective, the question is inaccurately or incompletely framed as some of the strongest firms globally are the principal obligors, thereby ameliorating most, if not all, of the inherent risk.

The Expectation

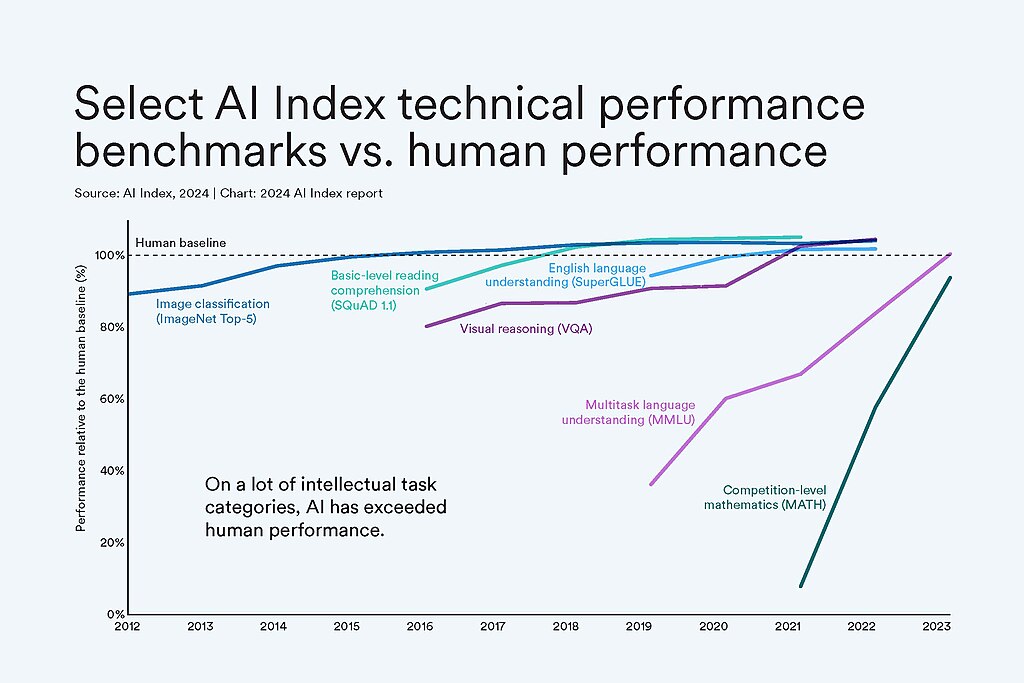

If Artificial Intelligence (AI) lives up to only a fraction of its promise, it will forever change the world, hopefully for the better. Research and development across industries will accelerate, costs and speed for operating enterprises will improve, and much drudgery will be eliminated. Below is some support for the benefit, even though we are in the early stages:

The below graph appears directionally correct.

The Obligors

AI has become THE topic of most technology-based firms over the past several years. The notion is AI will become embedded in nearly every facet of activity needing thought. There is a race to build out the infrastructure or be over-taken by more effective firms. At the forefront of this race are the biggest and best (i.e., the most credit-worthy firms) on the planet.

Concern I: Dot Com et Alia

The concern among many observers is that AI follows in the footsteps of many other technology innovations whereby the technology does in fact lead to massive improvements but that many of the participants suffer. Additional analogies are drawn from the tech bust (the Dot Com Bust) of March 2000 whereby the “Nifty Fifty” collapsed after massive run-ups in share price.

Concern II: Deep Seek

Deep Seek, a Chinese model, surprised many in the tech space by performing at the same level or even better than existing models but at relatively modest prices. While there is always the expectation that technology will improve, most informed observers expect the need for centers will remain robust.

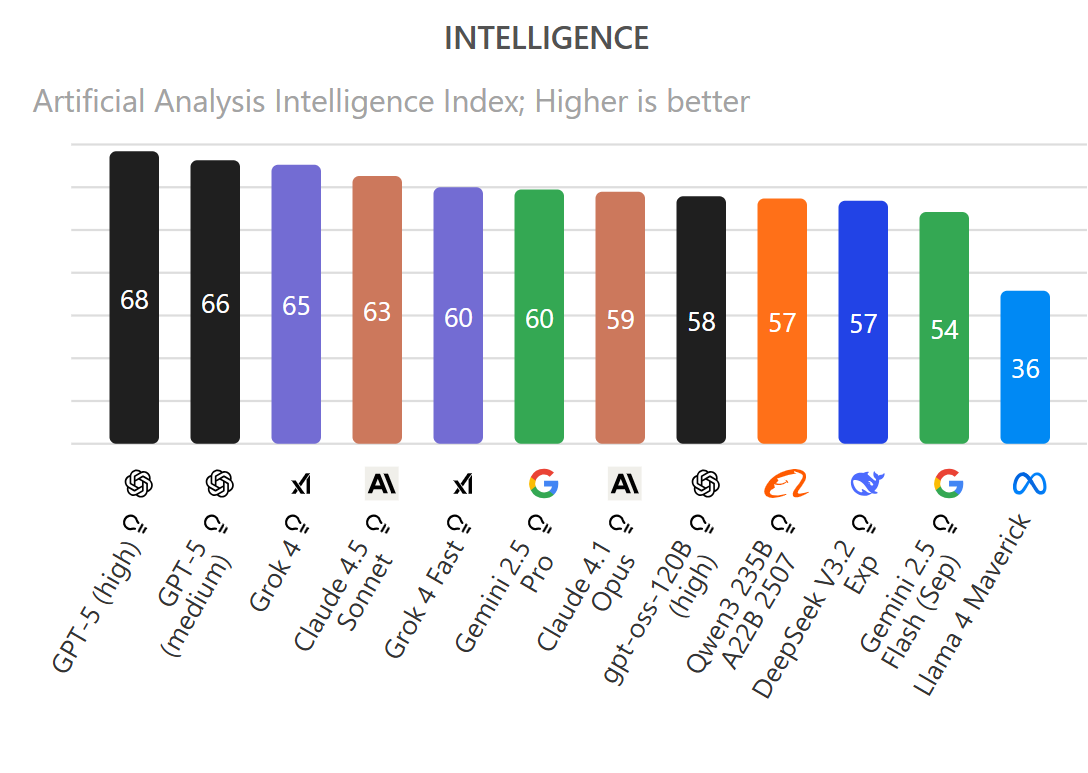

Another major disruptor is Grok, the AI model developed by Elon Musk’s xAI. In just 2 years, xAI has developed the third most intelligent model according to ArtificialAnalysis.ai.

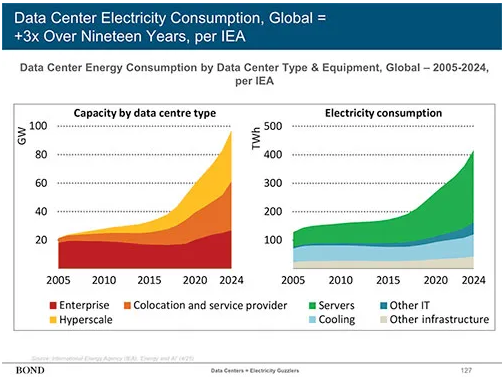

Concern III: Power & Water

Another challenge for industry participants, in addition to finding suitable locations for data centers, is arranging electricity to power the centers and water to cool them. (Note: The data centers used for model building and testing (i.e., Training Data Centers) can typically be located away from major metros whereas those used for the delivery of results (i.e., Inference Data Centers) need to be closer to metros.

Local electric utilities typically need years to expand generation capacity and often use traditional means for generating such power, which is typically at odds with the demands of the rapidly evolving tech businesses.

Hence the need for stable and easily scalable energy sources, notably nuclear (see Microsoft and Three Mile Island). (Note, the US Army’s planned use of tiny nuclear reactors is likely to open additional options for data center developers.)

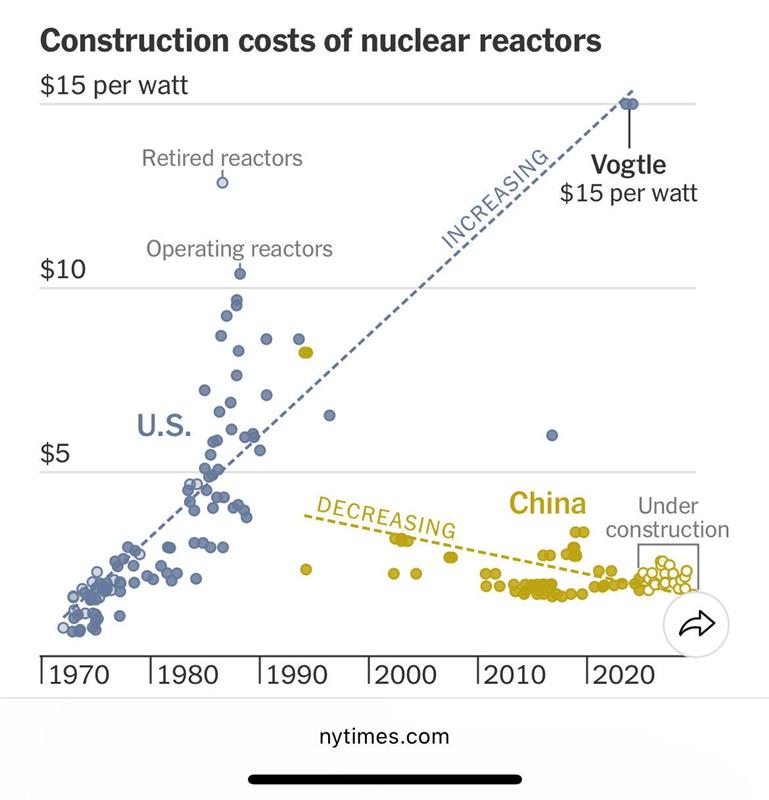

In this capacity, China has a massive advantage by producing energy at roughly 15% the marginal costs of new American reactors.

Given the critical need for power, being close to natural gas sources (e.g., Texas, Pennsylvania, Ohio, and West Virginia) is typically a material advantage.

An interesting development in the AI area is the need for speed, which translates into massive clusters for the data centers. The notion has a parallel in the computing field whereby the more transistors that can be placed on a chip, the faster and more productive that chip is (hence the need for even smaller and more powerful chips). There is a corollary in the data center area whereby the greater the number of connections, the more useful the center. (See Elon Musk’s coherence developments).

Concern IV: Chip Availability

Several quarters ago, firms were clamoring to get the latest and greatest chips, which were typically the latest chips from industry leader Nvidia. This concern has been ameliorated as Nvidia has ramped up production and viable alternatives have emerged. While chip availability is something to watch, it is currently not a major constraining factor.

Some Perspective

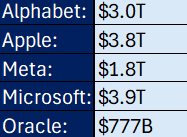

While all this discussion is interesting, from the perspective of creditors, while relevant, it is dwarfed by the fact that the typical obligors are quite capable of meeting their obligations regardless of the prospects of various data centers. Below are the valuations of some of the leading obligors in the space:

Providing further comfort is that the demand for data center space is far exceeding supply, translating into a bull market for any existing or slated projects.

Conclusion

It is always worthwhile checking assumptions. Nonetheless, periodically, the markets give gifts to those who are well-positioned and alert. Perhaps this is an area where risk is limited because of the strength of the obligors and the strong demand for the asset relative to supply.