.svg)

Off-balance sheet financings were the stated reason for some of the largest collapses in corporate history. And yet, they are with us today. The issue facing sophisticated institutional investors and risk managers is whether some latent risks will soon become more widely apparent, and what to do about it.

Enron and WorldCom failed supposedly because of their use of off-balance sheet financing which made the parents’ financials appear far more attractive on paper than they were in reality. (In our view, both firms failed because of underlying business problems, and the off-balance sheet financing was a symptom of a larger problem.) When the general market became aware of the problem (we flagged such via our junk-level credit ratings), both firms saw their financing sources retreat and their shares plunge. Note, the purpose of this installment is to highlight some of the major issues facing various firms in the industry; consult our rating reports for a more complete analysis.

Lo and behold, off-balance sheet financing is alive and well with some of the most well-regarded firms on the planet. The Tech Stalwarts are using the mechanism to assist in funding their buildout of the next massive tech upgrade. The culprit is AI (Artificial Intelligence), which appears to be affecting everything in the modern world and has the potential for upending everything in its path.

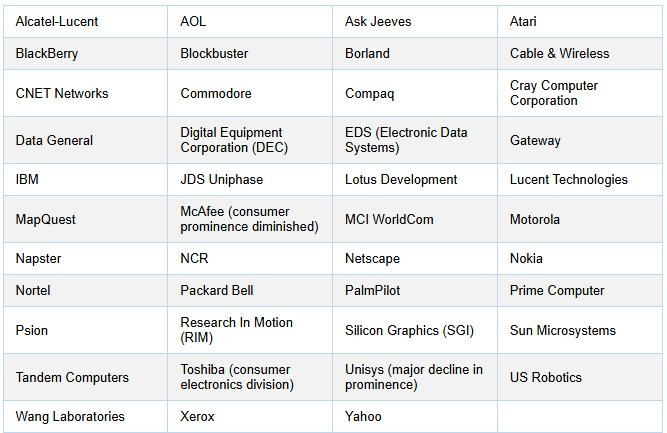

The “Bet” that firms are making is that AI will be a core technology and that if a leading tech firm does not have a significant presence, it has a good chance of being over-run. Examples of major shifts in the tech industry are numerous, and major brands such as DEC, IBM, Sperry, Burroughs, and a raft of others have either faded or disappeared as a result of those shifts (see the Appendix for a more complete listing).

The flip side is that the investments being made are enormous and could sink a firm if not properly managed. Additionally, there is the concern that the AI race might become similar to the search race, whereby, despite the presence of numerous firms over time (Firefly, AskJeeves, Yahoo, Bing, etc.), Google came to dominate the market with the others becoming less and less relevant. Supporting this notion is the development of the automobile industry, whereby over 1,800 domestic automobile firms were established since 1900, and now there are basically two legacy firms left and a few recent EV-focused firms (mainly Tesla, and smaller Rivian, and Lucid).

So, how big is the issue, and is it manageable? A reasonable way to spot the issue is whether there is a material spread between the reported net income and net cashflow. For starters, it is probably helpful to place the major participants in relevant buckets and assess how each bucket will fare in capturing value generated by AI.

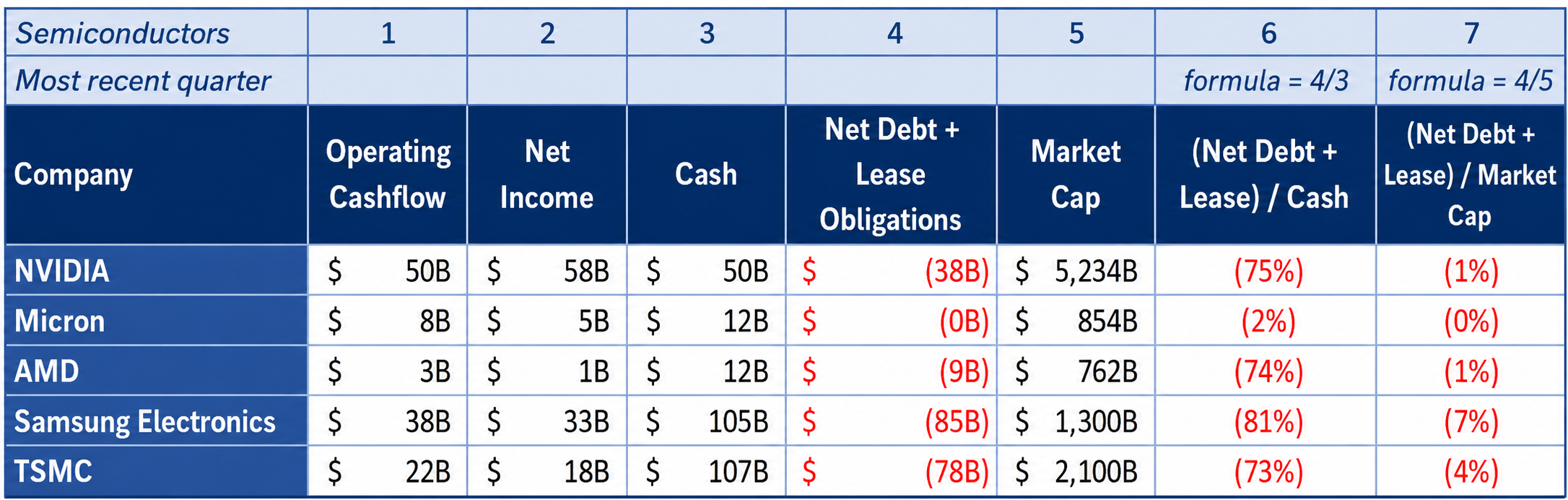

Below is a summary with the cashflow and net income for the most recent quarter. Figures are approximate:

A. Chip Providers - At the top of the heap in terms of risk/ reward (i.e., the highest reward with the least risk) for the AI revolution are the computer chip firms. Most have seen massive uplifts in their share prices and are likely to continue to benefit. The firms face ongoing challenges in remaining at the forefront from a tech perspective, but their balance sheets are generally considered to be fairly transparent and, for the most part, “bullet-proof.” Beyond the tech challenge, they might face some disappointment from the valuation of shares they absorbed in lieu of cash from the major Tech Stalwart firms, but for the time being, those risks are manageable. Below is a summary ($B except ratios).

B. Broad AI Providers – These are the firms producing the LLMs (Large Language Models) and other AI tools. Currently, there is a fight for dominance in the broad market. While the basic notion is that bigger is better, the DeepSeek model supposedly proved that it could produce respectable results with relatively little investment. The contrary notion is that it inappropriately obtained data from one of the larger firms.

Most of the AI providers appear to have two common traits: massive equity valuations and minimal (if any) profitability. Since most have used equity financing from the venture capital firms and in some cases tech giants (OpenAI is owned by Google Owner Alphabet), the risks to fixed income investors are minimal. Below is a summary ($B except ratios).

The critical question is whether there's room in the market for multiple players. Certainly there's room in the market for multiple models, which vary based on speed, intelligence, and cost. The massive upfront investment and rapidly changing model leaderboards have distorted the view of what can be achieved long-term. This picture is further complicated by potential future regulation.

By way of analogy, despite creating massive value for customers, car manufacturers and airlines have struggled. They have been hampered by stiff competition and high capital requirements. However, those industries don't have the same pressure as AI toward a winner-take-all model.

C. Tech Giants – This is the area worth some attention based on the concern over the commitments taken on by these firms. Below is a summary ($B except ratios).

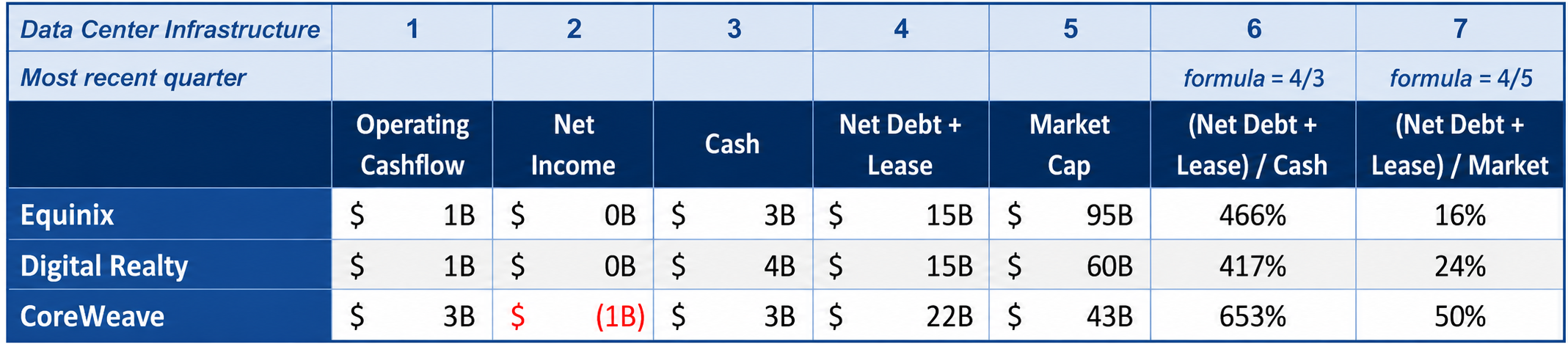

D. The Data Centers – The risks taken on by the data centers beyond the normal operational risks are whether the lessees (for the most part, the Tech Stalwarts) will continue making their payments, and whether demand will remain after the leases expire. To date, demand has far exceeded supply, but the risk remains. Perhaps the greatest source of comfort is derived when the centers are well-located with reasonable operating costs. (There is talk of space-based data centers, but the lifting and maintenance costs appear to outweigh the energy and water benefits.) Below is a summary of the major firms ($B except ratios).

E. Synthesis with Hardware/ Narrow AI Providers – This market is beginning to appear and is worth watching. The internet was developed in 1969 (via the ARPANet), but it wasn’t until a few decades later that the current tech giants evolved, enabled by the internet.

Regardless of the developments in software, AI requires hardware. Perhaps in the short term hardware providers such as Apple may sidestep some of the uncertainty, while maintaining exposure to much of the upside. For context, Apple's share price is up ~50% in the past year while Microsoft's is down ~10%.

There has been significant discussion of the AI sector, its implications, and attempts to identify winners and losers. From a credit quality perspective, there are a few which probably need more attention. Perhaps our major concern is the winner-take-all aspect for some areas. We believe we will soon be entering the second phase of the AI Revolution whereby narrow AI providers and synthesizers (i.e., using robotics and other hardware with AI) will create broad and interesting markets. Watch for who will be the owners of software, hardware, or both. NVIDIA, Apple, and Tesla each own both. Meta and OpenAI have made attempts to own both.

Perhaps the real winners will be the users of AI to make life easier. (See the photos at the top of this report for examples.)