.svg)

Overview

The major theme over the past couple of years has been what Niall Ferguson has labeled “The New Cold War.” The manifestations of this struggle have been Russia’s encroachment on the West via the Ukraine War, and to a lesser extent, the multi-faceted battle with China. While many enter wars optimistically, quickly that optimism translates into tears for both sides. Our fear is that the follow-on effects of the New Cold War are being ignored and will be long-lasting. From the perspective of institutional investors and risk managers, we will try to identify some developments that are likely to shift the environment for decades.

The Threats

While many discuss the risks associated with engaging a nuclear power, the probability of conditions devolving to the point that such weapons are unleashed is minimal for reasons stated in a prior installment. In short, any country using nuclear weapons would become a pariah for decades in addition to being vulnerable to attack itself. The bigger issue is the conditions which are likely to exist over the next couple of years. To address these issues, we will break it down into the Eastern Europe and Asia arenas.

Eastern Europe

The Ukraine War has continued for over three years with the battle lines being mostly static over the past six months. Masking this apparent inactivity have been massive changes behind the front lines. Of late, Ukraine has successfully attacked Russia’s energy infrastructure to the point that generating revenues for both war operation and standard of living is becoming problematic. Without both the fuel and the revenues to maintain operations, Russia’s ability to hold lines becomes imperiled. (Hopefully Russia’s difficulties might temper China’s coveting of Taiwan, but probably not.) On the other hand, the war’s sunk costs — the loss of life and treasure — translate into extreme difficulty in effecting a withdrawal. We have been here before with Russia’s actions in Afghanistan, which was a national embarrassment preceding the collapse of the Soviet Union. Given Putin’s age of 72 years, perhaps it is just a matter of time before he cedes power.

Assuming our premise is accurate and that it will be increasingly difficult to maintain the war effort and one way or another Putin is likely to step down over the next several years, where does that leave us? Unfortunately, typically, bad things happen to weakened countries. Ukraine will need a massive rebuilding, and Russia is likely to face a power struggle. Note, it already faced a brief, failed coup attempt by the Wagner Group in 2023. From an investor perspective, given the rather isolationist approach of the current administration, the vacuum left in the aftermath of the Ukraine war is troublesome.

Asia

For better or worse, China has been viewed as the major threat to American power for the past decade or more. The response has been a pushback on numerous fronts, with the most prominent probably being tariffs, Panama Canal port control, TikTok control, Nvidia chip sales, and more recently H-1B visa fees.

While many are focused on countering China’s rise, a missed question is whether a much-weakened state is in everyone’s interest. In our opinion, a fulfillment of the dream will carry a high price. For starters, China has been a major engine for global growth. A significant decline in GDP is bound to have spillover effects.

Looking for historical precedents, the one which comes to mind is Japan’s economic miracle , whereby the Imperial Palace had greater value than the real estate in the state of California. The miracle gave way to several lost decades, a situation which Japan is still trying to exit. Typically, super-heated economies burn out over time, and some early indications in China are worth reviewing. The property collapse, the over-investment in various industries and the faltering tax revenue are all areas of concern. Additionally, because of the massive level of state ownership, the normal market disciplines are lacking thereby creating major imbalances.

Western Europe

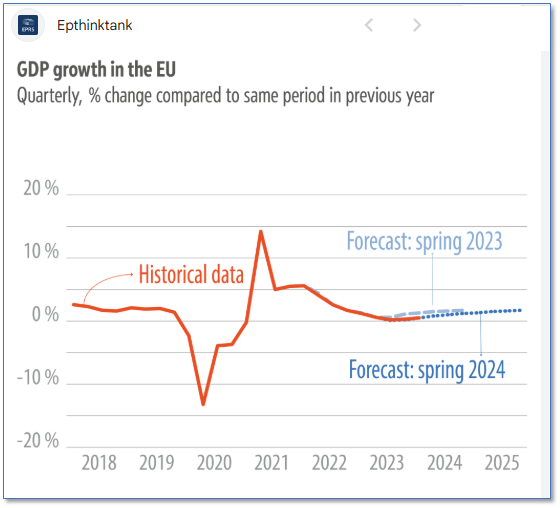

For those who have not been paying attention, Western Europe has changed massively over the recent past and is entering a phase where recovery might be increasingly difficult. Perhaps the best indication of this is the anemic growth.

From a historical perspective, the decline has been sobering; the source of massive innovation and growth over the past century is now a shadow of its former self with, on an adjusted basis, the continent has relatively few global leaders with exception in biotech (Eli Lily, Pfizer), the chip machinery (ASML), consumer goods (Nestle and Unilever), aircraft (Airbus), and banking (UBS and Barclays), autos (although their dominance is slipping) and probably a few others.

In terms of how Western Europe factors into the major shifts going on, perhaps the short answer is that to a far greater extent than was previously the case, it does not. As a matter of perspective, US GDP rose 87% between 2008 and 2023. EU GDP rose 13.5%.

The EU was created to minimize the chances that the various European nations would go to war with each other. No wars have begun between EU states since 1993, though peace also may be enforced through NATO and American hegemony.

As an effective force for change, the union is less united, as evidenced by decisions over defense spending, the continued purchasing of Russian energy, and moderate support for Ukraine. Given the anemic growth, the high level of sovereign indebtedness, and ESG concerns, perhaps the EU will remain in the background.

Upshot / Implications for Business

Three major points:

Paths Forward

At some point, the Ukraine War will end and the massive effort to rebuild the country will become an issue. Our view is that as usual, the current administration will weigh in with an emphasis on private support. At some point, Russia is likely to conduct a reassessment of the effectiveness of its extra-territorial activities and conclude the costs were greater than expected.

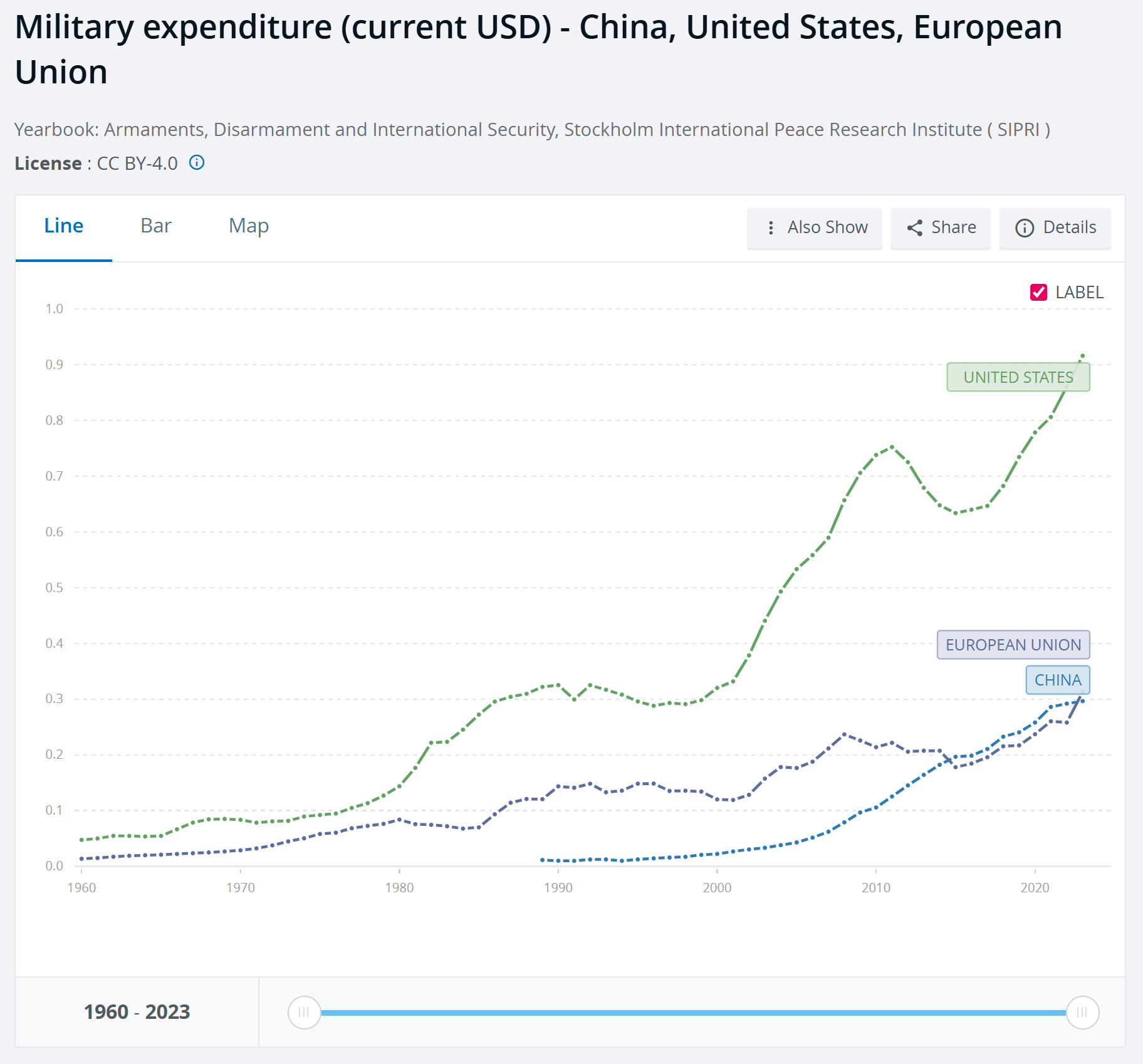

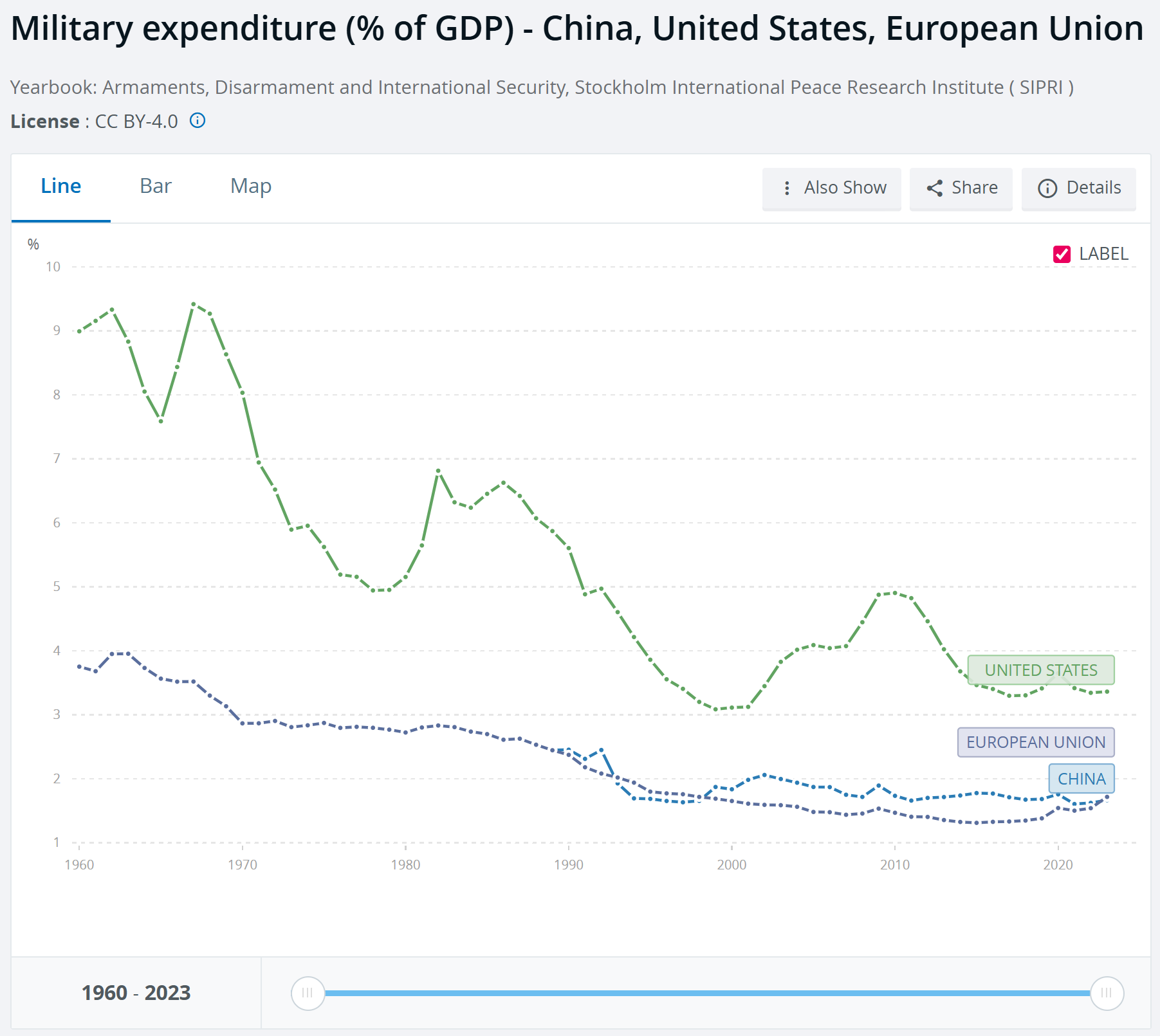

Concerning China, hopefully a level of detente will be reached whereby most nations can cut back the massive military expenditures and focus on other issues. It may be of some comfort that although military spending continues to rise, it has fallen as a percent of GDP for the United States, EU, and China. Though it may cause short-term spurts in economic output (as has been the case in Russia), military spending generally doesn’t improve long-term productivity or standards of living.

Conclusion

Businesses operate in the broader context of a political environment and that environment is massively shifting. Even over the past six months there have been massive changes, and our view is there will continue to be changes.