.svg)

The fixed income markets labor over finding the most accurate view of an obligor’s true credit quality. However, in our opinion, there is a far superior approach and that is a consideration of the fragility of ratings. As usual, our Risk Commentary is written with the aim of assisting sophisticated institutional investors and risk managers.

Lehman Brothers’ failure was the match which kicked off the most disastrous period for institutional investors in this century. Per Better Markets, the 2008 Great Financial Crisis cost $20 trillion, which is rather sobering as the figure is more than half the federal deficit. (Fortune Magazine named Egan-Jones Ratings number one for warning about Lehman and others and placed the Legacy firms in the aiding and abetting category.)

Revisiting the factors leading to Lehman’s collapse, there are three which come to mind:

The bottom line on Lehman was that a mere 1% decline in asset values was sufficient to halve its equity, but perhaps more importantly, cause its lenders to refuse to roll its liabilities.

Setting aside the issue of whether Lehman’s ratings six months prior to the collapse was accurate, a better approach for institutional investors and risk managers is the FRAGILITY of the obligor’s credit rating. In other words, if a small shift in conditions is likely to cause a material deterioration in the obligor’s credit quality, then investors need to know.

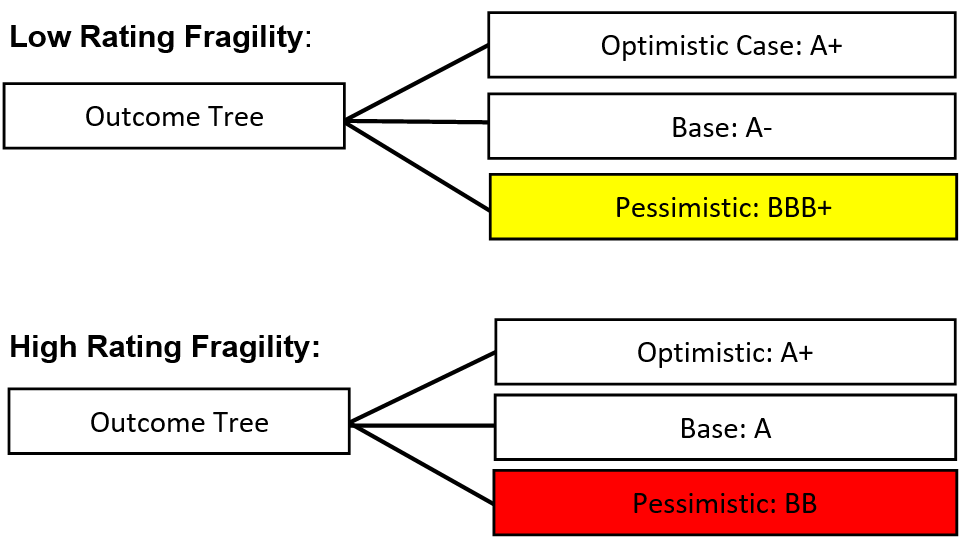

The best way of portraying this concept is to graph the likely downside for credit in various scenarios. In the case of Lehman Brothers, relatively minor deterioration in their financials was disastrous. Below is an illustration:

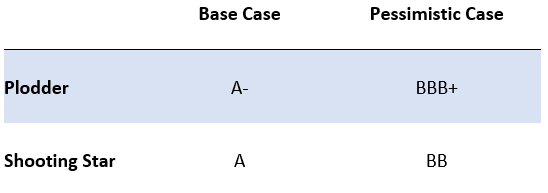

While it is likely that the Shooting Star will receive significantly more attention, from a risk control perspective, the Plodder is (i) a far safer bet and (ii) the spreads are likely to be more attractive. Furthermore, once the problems of the Shooting Star become known, liquidity often evaporates.

A Premise

While there is little doubt that obtaining an accurate read on the current credit quality is important, for the most part, this information is already reflected in the pricing. The item which can be disastrous for managers is an investment grade rating going bankrupt. We have recently had two reminders of this scenario in the collapse of Tricolor and First Brands¹.

From our perspective, fragility is critical but often overlooked. A manager is probably better off with a slightly lower grade credit which is resilient than a higher-rated credit which, in a reasonable scenario, has a good chance of going bankrupt.

Our reports currently address this concept in the 17G7 section at the back of the report but will be better highlighted in the near future.

A proper evaluation of credit quality should not be limited to a simple snapshot of current conditions but rather include an evaluation of reasonable (and perhaps unreasonable) conditions. This evaluation is important to all sophisticated institutional investors and risk managers, for without a sound foundation on the credit side, the equity side is in jeopardy. More attention in this area will reduce pain and lead to more satisfying outcomes.