.svg)

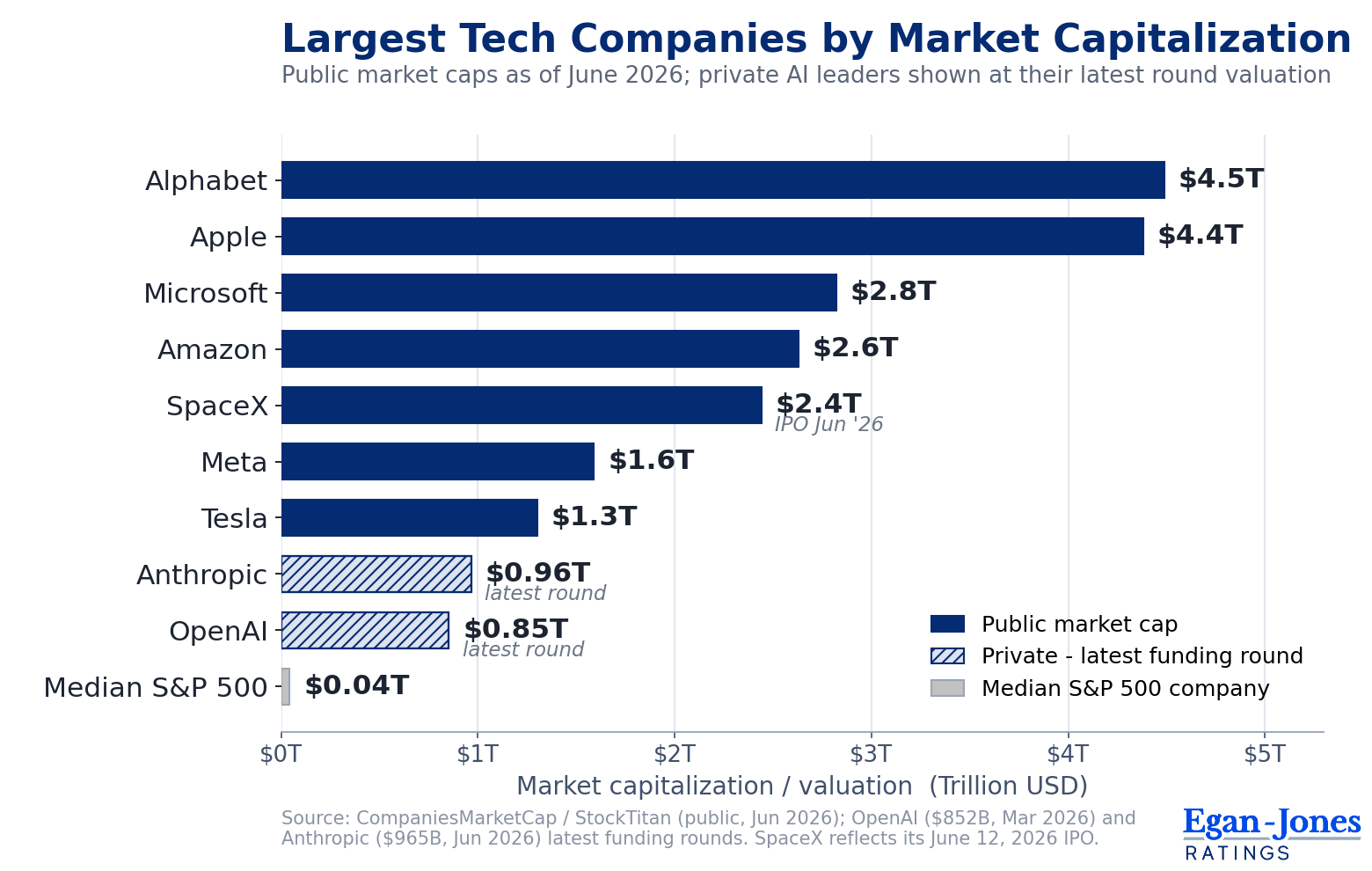

While the situation in the Middle East has dominated the news over the past several months, there has been another war waging with far-ranging implications. The Tech giants are embroiled in a fight which some consider to be an existential fight. Given the dominance of these firms, we aim to share a few thoughts which hopefully will assist sophisticated investors and risk managers in evaluating possible outcomes. The graph below underscores the relative importance of the tech giants.

Artificial Intelligence is expected to transform numerous fields:

“AI is one of the most important technological developments of our time.”

— Peter Thiel

There are a variety of other quotes, but needless to say, the Tech Giants and many others are heavily investing in the area.

Before addressing possible winners and losers, it might be helpful to understand that, like many emerging technologies, there are components associated with it that probably deserve discussion.

The Chip Firms - currently, these firms are the biggest winners, with Nvidia, TSMC, AMD, and Broadcom in the lead.

Data Centers - with demand for data centers far exceeding supply, and many (but not all) tech giants providing long-term leases, the sector appears to be in decent shape. The challenge for many is obtaining the components for building centers.

Power Producers - data centers consume tremendous amounts of energy for chip operations and cooling. Since most contracts match generation with firm usage obligations, there is risk here, but under current conditions it should be manageable.

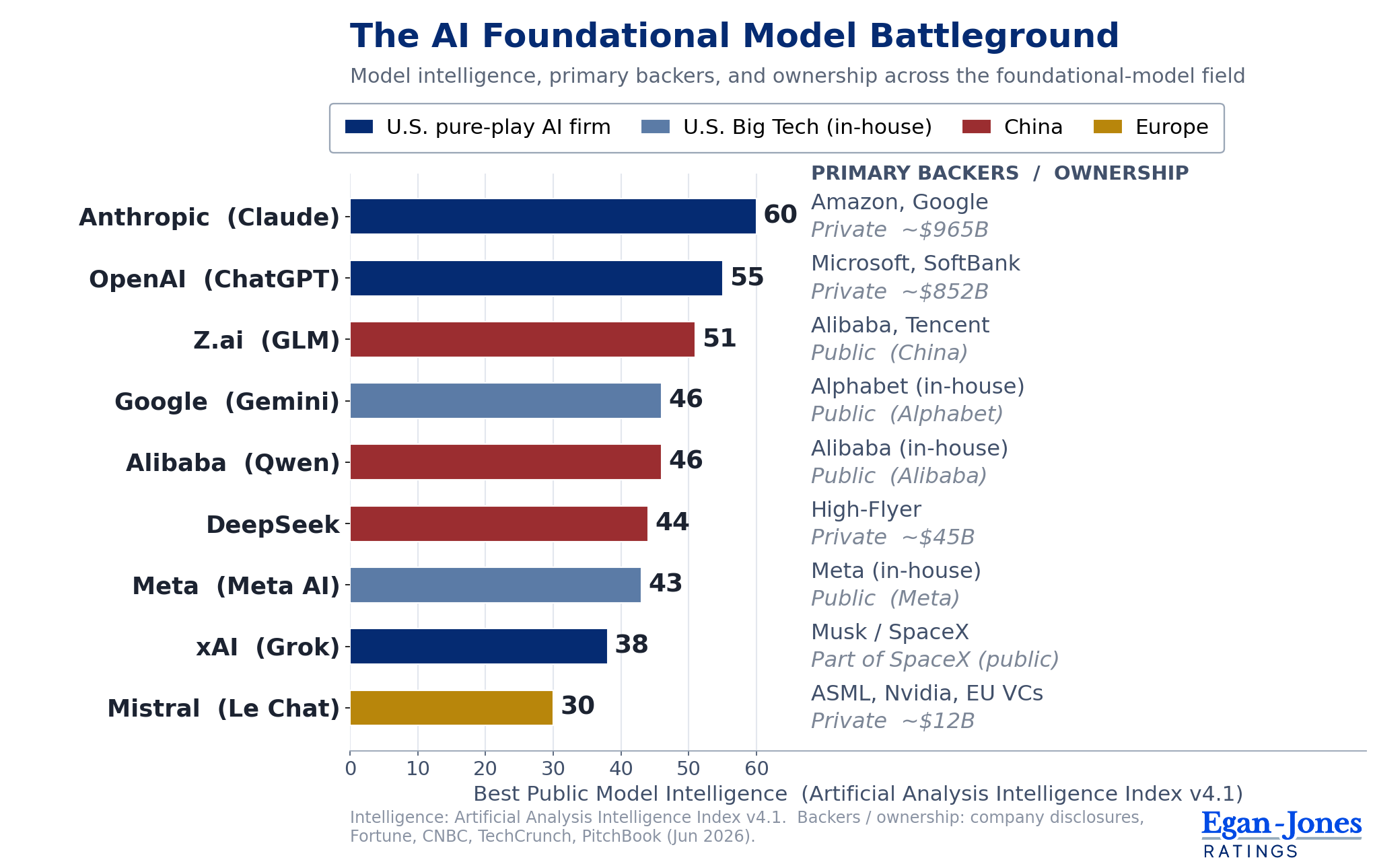

Foundational Models - the pure-play foundational model companies, whose core business is building the underlying models themselves. This is where the real battle is taking place and is worth some analytical time.

Hardware Producers - the makers of the physical devices AI runs on or through, such as phones and cars, where competition is intense.

Unlike the current business models of the tech giants, our premise is that the competitive landscape for AI is completely different. The chart below maps each major model's best public intelligence,2 its primary backers, and its ownership or latest valuation.

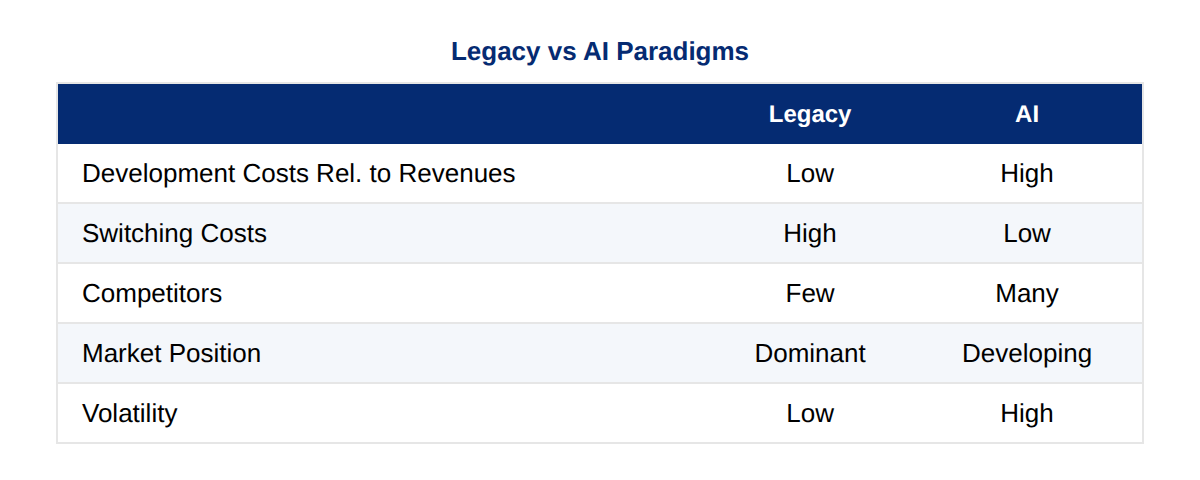

For Microsoft, META, Amazon, and Google, the previous paradigm was one of writing the basic code once and then extending it worldwide with only moderate competition from others. The switching costs were high and there were few viable alternatives. Below is a summary:

Given the purported (and expected) importance of AI, it begs the question of which firms have a decent chance of succeeding over time.

Our view is that the landscape will remain challenging, but that there are a few variables that are likely to become important over time. One is, obviously, the quality of models, and certainly Anthropic, with their Claude tool, seems to be in the lead currently. The others missed a few steps, but perhaps they can recover.

However, the item that perhaps is underappreciated by the market is the connectivity to the user. In this area, one would have to assume that those firms that control operating systems for mobile devices (Apple and Google) and personal computers (Apple and Microsoft) are in an attractive position.

Adding to the stakes is whether there will be one or two dominant firms which emerge. History indicates that, just as is the case with most hardware and software firms, the market will tolerate only a handful of firms, with the dominant firm taking most of the spoils.

Not addressed in this installment is the likely far more interesting and profitable area of combining AI with other areas such as advanced hardware. Close to the top of the list now are self-driving vehicles, robotics, and defense applications. Apple, Microsoft, and Google lag in these nascent areas, thus offering an opportunity for challengers, including smart glasses (Meta), gaming consoles (Steam), and robotics (Tesla and Unitree).

We suspect we will be returning to this area in the not too distant future.

A particularly strong position is to be the clear leader on one of three dimensions - intelligence, speed, or price. Each rewards a different kind of system, and each is winnable on its own. A few representative use cases for each:

Intelligence - being the most capable model on the hardest, highest-value problems. Where the quality of the answer is what matters most, the most capable model commands a premium.

Speed - turning very large inputs into the right output almost instantly. For real-time, physical systems, responsiveness is the whole game.

Price - delivering good-enough results at the lowest cost per task. For high-volume, repetitive work the cheapest capable model wins, because at scale the per-query cost dwarfs a marginal gain in quality.

A dose of humility is in order here, as the area is changing rapidly. Furthermore, the government(s) appear to be weighing in (see the news on Anthropic's latest model), which might further complicate outcomes. Lastly, there is the issue of garnering resources for training and delivering model results.

The world is changing rapidly. This installment aims to provide a framework of possible major shifts for the benefit of sophisticated institutional investors and risk managers.

1 Quote attributed to Peter Thiel; see the book excerpt in Wired (Keach Hagey, The Optimist: Sam Altman, OpenAI, and the Race to Invent the Future).

2 Artificial Analysis Intelligence Index v4.1 incorporates 9 evaluations: GDPval-AA v2, τ³-Banking, Terminal-Bench v2.1, SciCode, Humanity's Last Exam, GPQA Diamond, CritPt, AA-Omniscience, and AA-LCR. Scores reflect the best publicly available model from each company.

Chart, Largest Tech Companies by Market Capitalization: public market capitalizations via CompaniesMarketCap / StockTitan (June 2026); OpenAI (~$852B, March 2026 round) and Anthropic (~$965B, 2026 round) shown at their latest private funding valuations; SpaceX reflects its June 12, 2026 IPO.

Chart, The AI Foundational Model Battleground: model intelligence via Artificial Analysis Intelligence Index v4.1; backers and ownership via company disclosures and reporting (Fortune, CNBC, TechCrunch, PitchBook), June 2026.